Published October 10, 2024

Graham McKenzie: Good afternoon, everyone. For those of you who don’t know me, my name is Graham McKenzie. I’m part of the team at the TMX Group that helps facilitate our ETF business, and I want to welcome you to today’s exciting event hosted by Global X. Probably it is no surprise to see such a good turnout here in regards to sort of the events that are transpiring south of the border and how it’s going to impact us. I think we’re really set to really hear an engaging conversation. I’ve had the privilege of participating in a pre-call for this a couple weeks ago and seeing the banter go back and forth in the emails that followed, that as far as what is going to come in this conversation. So with that, let’s get going and get started and allow Chris to get started. And I’ll jU.S.t put one comment out here. We’re also at four o’clock going to close the market so you have that to anticipate and look forward to. With that, Chris, do you want to take over?

Chris McHaney: Great, thanks Graham. Thanks everyone for joining U.S. today. My name’s Chris McHaney. I’m head of investment management and strategy at Global X. We have an interesting panel discussion for you today followed by the official closing of the market as Graham mentioned. So hopefully a little fun after the discussion. Following on our company’s rebrand from Horizons ETFs to Global X, one of the initiatives we really wanted to put forward was investor education and thought leadership in the ETF industry here in Canada. So panel discussions like we’re doing here today go a long way towards that initiative and hopefully provide insight and perspective for advisors and investors when you’re making your own investment decisions. So hopefully you find this very valuable. JU.S.t a couple of housekeeping items. Graham did briefly mention it, but we’ll have the panel discussion. We’ll try and leave about five or 10 minutes for Q and A from the audience as well. And at about 3:55 we’ll make our way over to the big button for the official closing. So with that, let’s get started. I’ll have my three panelists introduce themselves and we’ll start with you.

Anu Ganti: Thank you so much. It’s so nice to be here in Toronto. My name is Anu Ganti and I run our U.S. Index Investment Strategy team at S&P Dow Jones Indices. So what my team does is really analyze indices, [00:02:30] provide thought leadership across our suite, both in the U.S. and across Europe globally. Very excited to be talking about the topic of the day, which is elections. I know we were joking earlier that we could talk for hours about this topic, which we won’t. We’re going to try to pack it in and keep it crisp, but really looking forward to the insights. Don’t hesitate to ask questions or find U.S. afterwards. Looking forward to it.

Warren Lovely: Great, thanks. Yeah, so my name is Warren Lovely. I’m a managing director at National Bank Financial. I work in our economics and strategy group, so that involves of course, having a view on evolving economic and financial market developments south of the border. So pleasure to be here, I think this is Chris, as you said, quite a good initiative. I’m pleased to be participating. Notwithstanding the reference to the pre-call, I don’t think we’ve got a script here, so I am looking forward to, I think, a reasonably dynamic and intimate discussion. Brooke?

Brooke Thackray: I’m Brooke Thackray, I’m With Global X. So I work with the fund HAC, which is the Global X Seasonal Rotation fund, and the primary mandate for that fund is seasonal, so that fits in with elections because we can talk about some of the cycles that actually happens with elections, how the markets behave before the election takes place and after as well. I’ve done extensive writing. I’ve written a number of books on seasonal investing over the years as well, and I also do a lot of media appearances as well. But I’m looking forward to today’s conversations actually, because it’s very topical and there’s going to be a lot of anxiousness coming into this election. There has been in the previous. ones, so it’ll be a good discussion of what might take place in the markets in Canada and the U.S. before the election and after. So it’s going to be quite exciting.

Chris McHaney: Alright, thank you. And yeah, looking forward to hearing different perspectives on some of these topics. So one thing I’ll jU.S.t ask you all to keep in mind as we are going through the questions, what we’re trying to do is analyze the impact on financial markets and the economy from the election. We’re not discussing pros and cons of particular candidate’s platforms or any party in particular. So trying to keep the political apart to the side and we’ll focus. on markets and economics if that’s okay. Warren…

Anu Ganti: That’s for the cocktails.

Chris McHaney: That’s right, yeah, yeah. Okay, let’s get underway. We’ll start with a question on if your analysis of the impact of the election has changed at all recently. We had the debate two nights ago. We’ve had of course change in candidates even from one of the parties. And so has your analysis of the impact of this election changed at all recently? If so, why or what caused that to happen and what is that thesis? Maybe we’ll start with you for this one, Warren.

Warren Lovely: Can I jU.S.t answer? Yes. Okay. So Chris, I think you jU.S.t hit on a couple of things and alluded to a couple of important respects. I mean this has been a pretty fluid election backdrop already. I’m not sure what the odds were for Harris Wall’s ticket start of the year. So we have seen [00:06:00] something of a bit of a roller coaster in terms of both candidates and earlier Biden in terms of the expected outcome, the likelihood and probability of winning. I would also emphasize that there’s still seven weeks to go. So as tumultuous. and interesting as the last number of weeks have been, we still have some runway to move down before we get to November 5th. So our analysis evolves with changing probabilities [00:06:30] on the election. Now, in terms of the original thesis that we had, I think there was a couple elements I would jU.S.t want to touch on quickly and then I can turn it to my fellow panelists.

So the original thesis would’ve involved that at a minimum the election would be entertaining and produce volatility. And I think that’s happened, I’m being a bit facetious. here. Other key elements of our thesis would’ve been both parties seemed to agree on protectionism. We’re seeing that I think reinforced both on issues like energy. We sensed a lot less divisiveness this time around than in prior iterations. In particular with the Democrats taking a somewhat more pragmatic view on oil production. We sensed that both candidates, both parties would be offering significant fiscal inducements to voters with differences in tax and spend policies. And that’s certainly been on display. We also feared, and this fear has been I think realized that neither party would talk about the deficit and debt and fiscal sustainability. This is the great issue that no one is talking about and maybe I sound like an old guy.

Brooke Thackray: Do you think that’s going to come up? Do you think that’s going to be important coming up shortly or is it jU.S.t a nonissue at all? Because the debate the other night, there was nothing…

Warren Lovely: Zero. Right? So I guess I think what it’s going to take is a couple events to galvanize attention. I guess maybe the January debt ceiling debate. And I think a lot of this Brooke is going to hinge on how much and how significant congressional control really looks across the party lines. ObvioU.S.ly if we have a clean sweep one side or the other, then we can make easier progress on things like the debt ceiling and so on. But all that to say, some elements certainly have changed consistent with this roller coaster of probabilities, but a lot of core tenants of our view remain intact.

Chris McHaney: Brooke, anything to add to that?

Brooke Thackray: Yeah, so I mean there’s been no economic discussion. So we’re talking about economics here, about what’s happening with and how it affects the markets. We can all, the problem is in trying to address the topic is everybody comes from their candidate so to speak, and they’ve got a lens that they’re looking through and they can look at exactly the same facts to different intelligent people and they’ll come up with totally different answers here. And it’s tough because they don’t go through costing at all on this at all. You’ve got some snippets in saying that this is what we could do, we might do this with the taxes or these are more sound bites than anything else. So nothing’s really changed in the whole process here. As far as the candidates go, personally, I think that both parties don’t really care about the debt. They haven’t talked about it, but I don’t think they care about it. And that’s a long-term problem. To me it’s huge, $35 trillion debt, 6.1% deficit to GDP, that’s unsustainable and there’s no sign of that slowing down and that’s the Democrats, but the Republicans will be no different and that’s disconcerting. So that’s longer term. I can’t tell you when that’s going to affect the markets overall, I jU.S.t can’t tell you, maybe it’s two years, maybe it’s three years, but it is a problem and it’s a problem that nobody cares

Chris McHaney: On that positive note. Thank you. Sorry…

Anu Ganti: There’s happy stuff coming folks.

Chris McHaney: Let’s maybe take a look back at some of the previous. elections and see is there anything we can tell from prior cycles? What has the impact been on markets? Does it matter Republican versus Democrat? And can we draw any parallels between maybe elections that were taking place during similar economic times as we have now? And Anu, I’ll start with you here. Yeah…

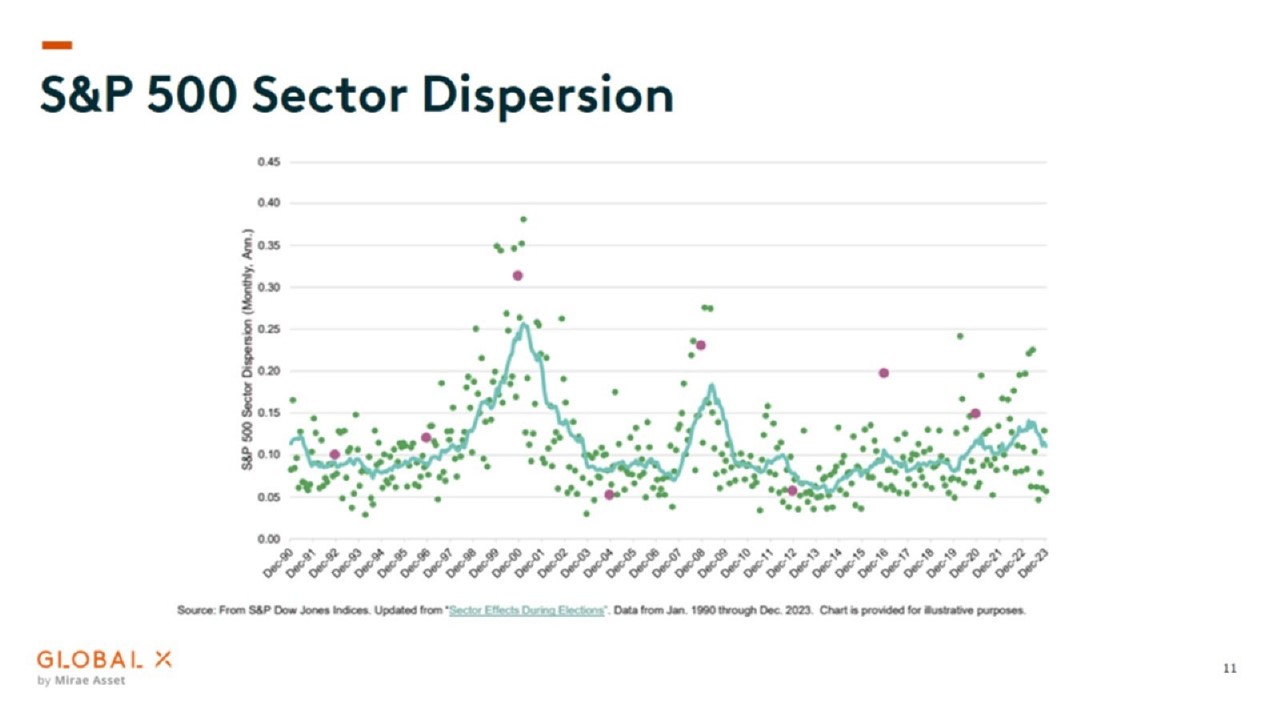

Anu Ganti: No, it’s a fascinating topic and in our history, in our research, what we found is that sector allocation could potentially be really relevant during this election regime. And the reason we came across this is through a measure you’re going to hear about volatility in a bit is through a component of volatility that we talk a lot about called dispersion, which what I mean by dispersion is jU.S.t cross-sectional volatility. If you have an index, jU.S.t measure the spread of returns in an index. You could do it at the stock level, you could do it at the sector level, you could do it at the country level. What you’re looking at right now is s and p 500 sector dispersion going back to 1990. You see a lot of dots here, but if you look closely, if you look at those blue dots, those are the presidential election November data points, most of them tend to be above average.

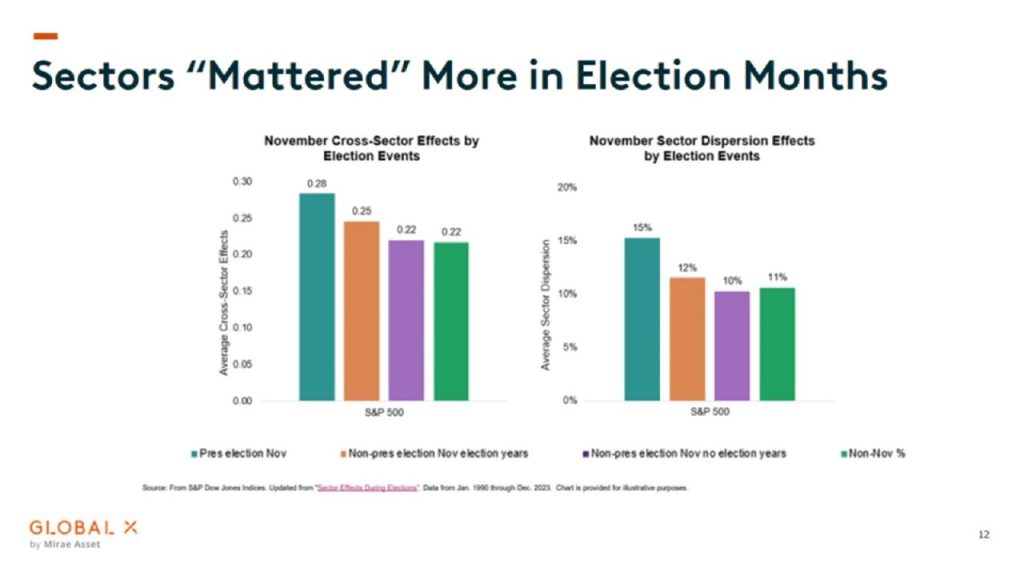

So that really stood out to U.S. and we actually took it a step further. If you go to the next slide, what we did is we broke our database into four buckets. So you had the presidential election Novembers, then you had the non-presidential election Novembers when you have the congressional elections and then you have the other Novembers, the non-election Novembers, and then you had all the other months the non-Novembers. And we looked at on the left hand side, the cross sector effects the average cross-sector effects. What I mean by that is how much of the market dispersion, how much of that spread is coming from sectors. And on the right-hand side, we jU.S.t took the spread among sectors, the sector aspersion. And what you see is a nice linear relationship where the cross-sector effects really mattered in presidential election. Novembers, no matter how you sliced it, whether you looked at cross-sector effects or whether you looked at average sector dispersion. So that stood out to U.S. and what that tells U.S., the intuition is there’s greater opportunity to add value from your sector picks if you are right. I will add that there’s that caveat if you have the skill, so if you think about sector rotation strategies for example, that’s something to pay attention to. So that was one of the key takeaways from our research jU.S.t looking at history. I will caveat that every election is different, so we’ll see what happens this time around.

Warren Lovely: Yeah, can I just piggyback on that because full disclosure, so I’m an economist by training, so I get into like empirical analysis as part of my kind of bread-and-butter approach. But I think at the same time, and Anu just touched on this, you need to be a little bit careful drawing inferences from the historical record. I mean looking back, empirical analysis can tell you everything and nothing at the same time. And what I mean by that is as Anu jU.S.t mentioned, you have to control for a lot of aspects. What’s a representative presidential election really look like and is 2024 representative, I would argue not at all. It’s hard to in fact really pin down what is or what was a representative election.

Just even consider the contrast between now and where we were last vote, right four years ago, right in the midst of a global pandemic, global economy shuttered U.S. unemployment rate at 7%. Inflation, non-existent interest rates at the extreme lower bound, the fed buying anything it could find to provide the most extraordinary support. Four years later we’ve got an economy in a vitally different position with monetary policy interest rates in particular, not at the effective lower bound, but in really punishing restrictive territory. So again, an economist is always going to tell you when they do this type of empirical analysis, they’re going to have that caveated on there, “ceteris paribus” all else equal. And man, there’s a lot to control for here.

Anu Ganti: There totally is. And as you were speaking, one other point I wanted to allude to is this is all for the S&P 500. I’m sure somebody’s wondering what about the S&P 400 or the 600, what about the mid- and small caps? How does it look there? We did look at it and what we found is there the power was actually strongest for congressional elections where we saw the greatest cross sector effects. So that sort of gave U.S. a thinking like perhaps congressional elections, more domestically sensitive stocks where we saw the power of the sectors come through mid in small caps, which really goes to the point that again, not all elections are created equal. It could differ depending on what you’re talking about.

Brooke Thackray: Anu, when you looked at this, did you break it down into when the party changed hands so the incumbent party did not…

Anu Ganti: Excellent question.

Brooke Thackray: …get power? Because I imagine dispersion would increase.

Anu Ganti: You are absolutely right. I think that’s one area of future research. We could definitely look at that, right? Was the incumbent power, was it depending on who was president? Was it the house or the senate that had the lead? There’s a lot of different ways that you could slice this research. I know I’m skipping ahead a little bit, but if you’re wondering does this also take place globally? We’ve had so many elections. I know the topic is the U.S. election, we’ve had elections all around the world. We’ve started to look at this including in Canada. We see a very similar result there as well.

Warren Lovely: You might need to accelerate your work on the Canadian election.

Anu Ganti: Exactly.

Chris McHaney: Okay, great. Thank you. I think it was mentioned a little bit earlier. Historically U.S. elections are involved with greater volatility in the equity markets. What strategies can an investor consider to maybe mitigate some of that volatility? But also we know volatility also creates opportunity, so take advantage of opportunities as they come up as well, both going into the election but then also coming out the other side. Anil, we’ll start with you again.

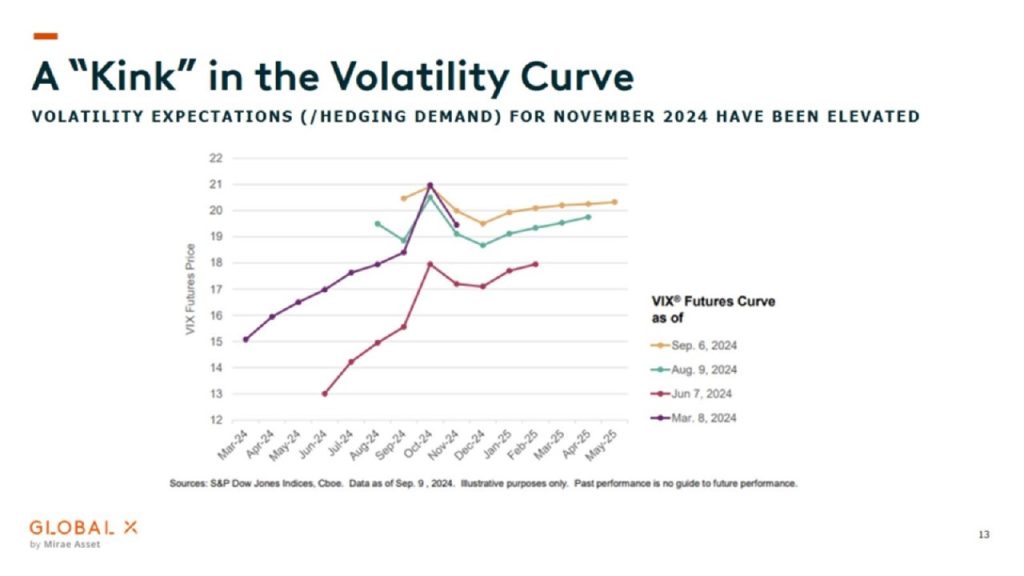

Anu Ganti: Yeah, so the word volatility is interesting, right? So many different ways to define volatility. We just talked about dispersion, which is a component. There’s also measures of volatility expectations or implied volatility. And we’ve got a slide here. This is just fascinating to me. You’re looking at the VIX futures curve, a little bit of background. So VIX is a measure of implied volatility over the next 30 days. The VIX futures curve shows you where the market expects VIX to be trading at, and it usually has this sort of boring upward slope. But around the October timeframe you see that kink, right? That kink in the curve and the way to sort of interpret that is sort of the market pricing in this idiosyncratic risk, right? What’s going to happen? We’re not sure increased demand, increased hedging demand. So this is something that we’re closely watching on the desk to see expectations for volatility.

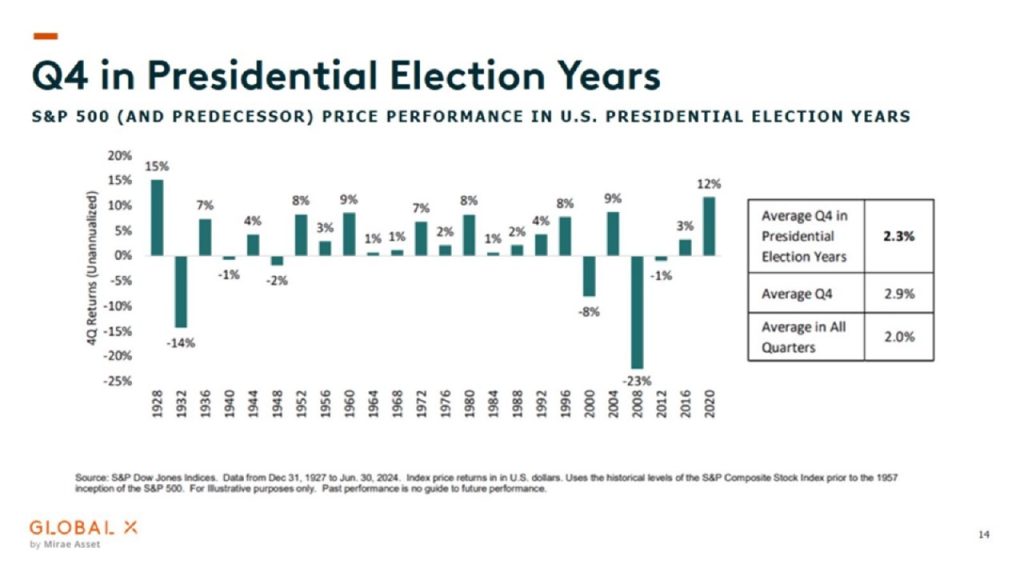

So that’s one side of volatility. There’s also history and realized volatility. And going back to the earlier points that Brooke and Warren were talking about, we dialed in on Q4’s. I think there’s a slide coming on historical Q4s in presidential election years where election happened, how did the market process it? What happened in the aftermath? And you can see there’s a lot of chop, right? There’s no clear linear direction one way or the other. The average Q4 in presidential election years was 2.3%. The average Q4 was 2.9%, right? So not a huge difference there. I’m sure we’re all remembering 2016 and 2020. We saw the move upwards in Q4. So history is a guide, it’s not perfect, it’s a guide, but that’s something that we’re looking at from the volatility side.

Warren Lovely: I think the other thing need to just bear in mind and looking at your VIX futures curve, I mean there was the presumption of course that we would kind of get through the summer quiet time and then the volatility is going to peak because we get close to the vote. And of course that’s exactly what the empirical [00:18:30] average path shows you. Maybe we weren’t fully discounting bouts of volatility like we saw in early AugU.S.t when carry trade, the unwind and fear of that sparked periods of volatility. I think what I’m trying to say here is that there is the election narrative, but it’s hard to disentangle and fully detach it from the broader global economic narrative that is itself characterized by [00:19:00] immense uncertainty and volatility. And without being too cryptic, what’s the type of positioning you do in an environment of decelerating global growth, rapidly deteriorating economic conditions in the U.S. labour market?

It’s defensiveness in my view, not just to protect against an anticipated bout of short-term volatility, but to protect yourself from what could be a much longer lasting slowdown in the U.S.. And again, without getting too much into our macro view on the U.S., I can tell you that developments in the U.S. labour market look particularly disconcerting. I think the weakness that we’re seeing emerge in the labour market. It was anticipated this time last year. It’s observed, it’s real now. It’s going to impact investor philosophy before the vote of course. And I think in the aftermath of the vote as well,

Anu Ganti: I totally agree with that. You’ve got so many macroeconomic uncertain variables right now. Everybody’s talking about the yield curve and the version we saw the better-than-expected U.S. CPI numbers. There’s a lot going on.

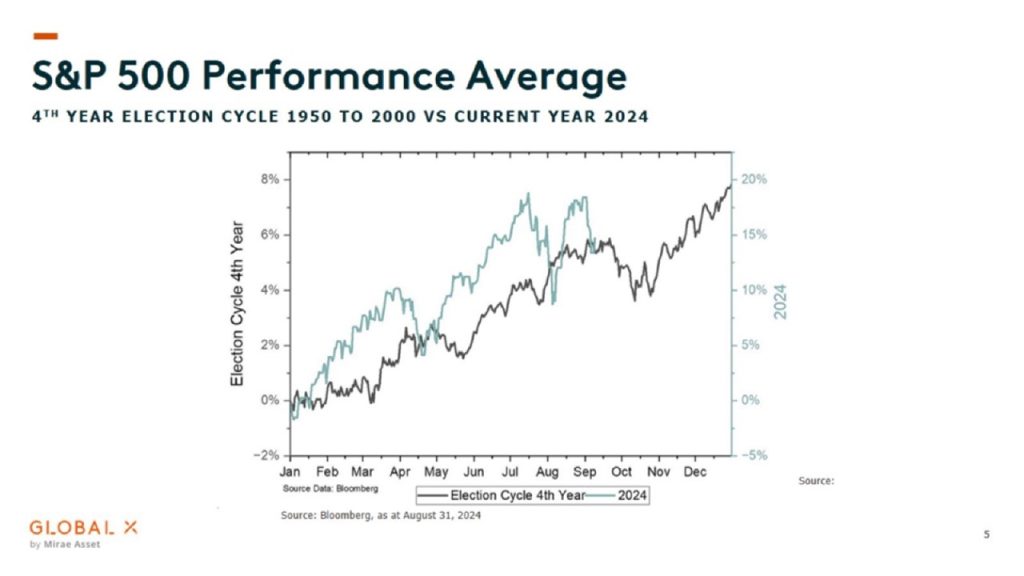

Brooke Thackray: There is a lot going on. But I do think that a good place to start and is to look in the historical context of what’s happened and Warren’s right every time’s different and we can talk about those exceptions. If we took a look at the, I’ve got a graph here that shows the average fourth year seasonal cycle for the markets here. So that’s the black line. Now the Y axis on the left is different than on the right now the teal line there is 2024. That’s where we’re at right now. And that’s the axis on the right. So it’s not the magnitude of the moves, it’s the direction of the moves here. So that black line shows you the average trend for fourth years of, so the year we’re in right now for election cycles coming into the election. And it’s important to note that what we typically see is we tend to see some sort of bottom take place jU.S.t before the election happens.

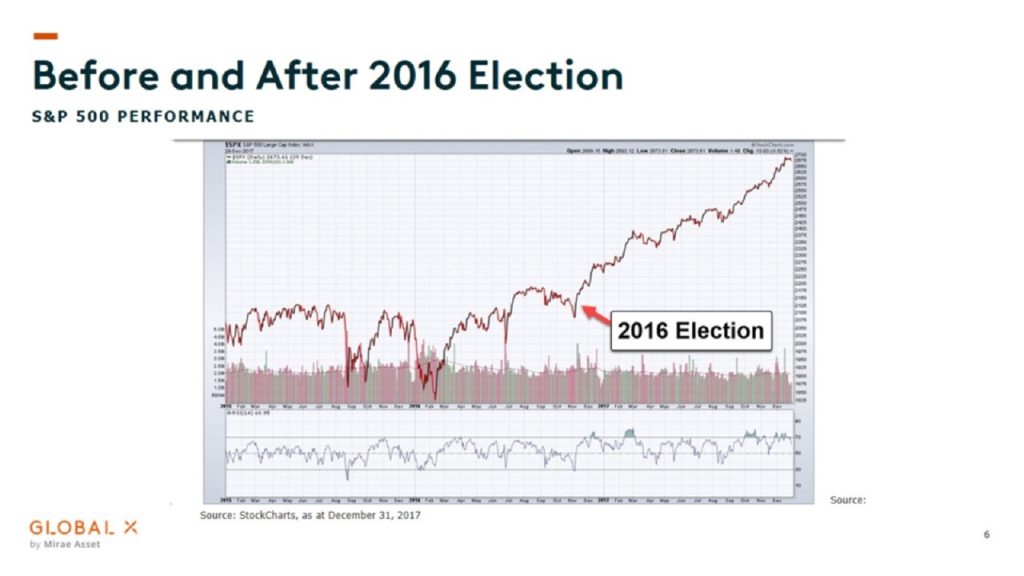

And that happens on a fairly regular basis. Why would that happen? It’s because there’s a lot of anxiety that takes place in the market. Everybody’s investors are saying, well, I’m not sure who’s going to win what their policies are going to be. And you tend to find the market will tend to correct down into that. So far this year, by the way, seasonally, we’re actually very close to that tracking line here as far as that goes. But then the market tends to bottom before the election and tends to rise after. And as Warren mentioned, 2016 we saw that runup in 2016 after that. Now that was a strong runup. I’m not sure that’s going to happen this year, but let’s go back and take a look at 2016 and this is the election that took place and the reason why I’m choosing this, that was the time that Donald Trump was running.

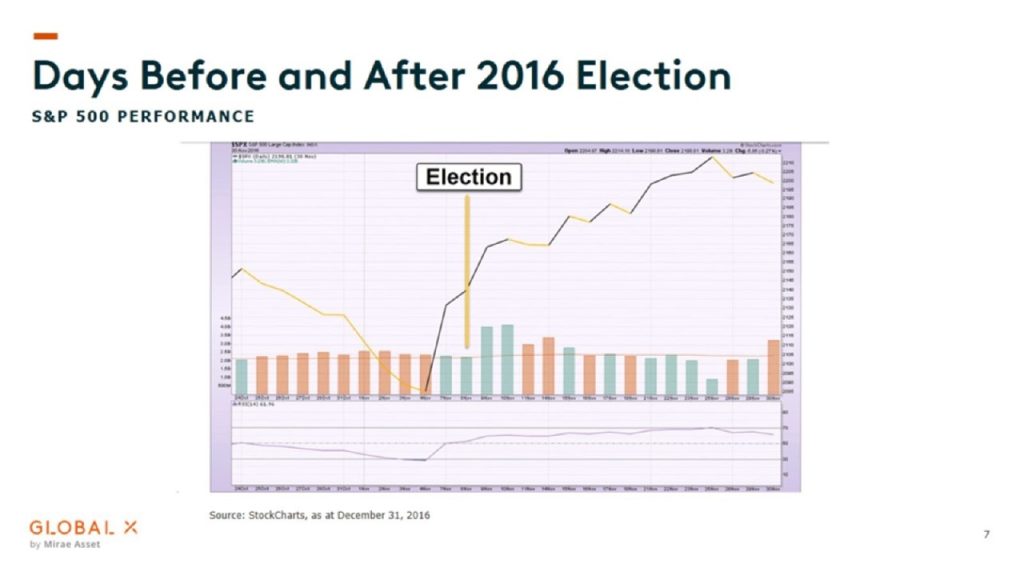

And if you take a look at the S&P 500 heading into the election, everybody was going: “Oh, Donald Trump, he’s an unknown factor”. Investors don’t like uncertainty. And they were pushing the market down substantially coming into there. And we saw that correct sharply into the early November. And then we saw that rally basically a couple days before the election take place and then we saw the run right into the next year. But if you go to the next chart, you can see that bounce that took place there was the election and two days beforehand, the market all of a sudden bottomed. He said, look, we got all that anxiety out of the way and now we’re looking forward to the future. So there’s going to be a lot of anxiety coming up in this election, whether it’s Trump or Harris, but the reality is a lot of that’s going to get worked itself out before the actual election takes place.

And I don’t know what the market reaction will be. Nobody expected or very few people expected the market to react so positively back in 2016 if Trump was to win, but all of a sudden the narrative flipped like that. So I can’t say that this is going to happen for sure. If we go back and look at similar times back, let’s say a similar circumstance, 2000 the year 2000, right? So here we had tech way above everything else. We had completed values in the market. We had the federal reserve had was raising rates. So we were very similar in a lot of ways. There are differences of course, and that was a bit of an exception. So we saw the feds start stop raising rates in May of 2000 and then at 6.5% then we saw the market’s peak in August and then November, that was when Bush got elected.

Then we saw the markets actually correct. So in that case, what we did see on that election, we saw the markets actually go down a bit right after. So it actually went against the seasonal trend or the typical trend that takes place because of factors. And I will say we are a little bit like that in this scenario right now. I had say we’re very close to it. I’m not going to talk about the tech stocks and the valuation, but we’re just as far as the rate hike cycle happening and extended market taking place as well. So maybe what we see this year is we do see a little bit of not such a strong rally after the election takes place as we have seen in the past. And that’s not a good sign. If we don’t see a strong rally in the market after that could be a good sign that the market’s in trouble. I mean I would expect at this point that maybe we would see the market rally despite if it’s Harris or Trump getting in that we’d see the market rally coming into the end of the year. And I think we’re probably going to at that point, that honeymoon’s over and we’ll see what happens from there.

Warren Lovely: Yeah, I might take the under on your stock call. Personally, my fear here is not withstanding the analysis that we’re doing here in the commentary or on the election, there is this broader cyclical story that is jU.S.t impossible to look away from right now. And what that story is telling you, you kind of shout it from the rooftops at this juncture is that the U.S. labour market, that great bastion of economic resiliency is cracking. It’s giving way a lot quicker than we had thought. So again, there is the anticipatory nature and the hope that we’re going to get to lower interest rates and that’s going to salvage growth and restore confidence and provide renewed vigour for equities. The reality is I think we’re going to be faced with a very difficult 2025, regardless of which candidate carries the day, regardless of whether it’s full or partial control of congress. Obviously, the specific tax and spend policies, corporate income tax policies and so on are going to have varying impacts on earnings profile and the like. But the broader backdrop here is somewhat concerning.

Brooke Thackray: I totally agree with you on that totally. My point was that we typically have a strong rally, a very strong rally in November and December for the stock market and maybe we get that, but it’s probably not going to be as much because of the cyclical backdrop that tends to be weak at this point.

Anu Ganti: It’s sort of going back to that Q4 chart, right? You see the bump and then who knows what’s going to happen after that.

Chris McHaney: Okay, moving on to sector perspective, certain sectors like technology, healthcare, energy tend to be a bit more sensitive to policy changes, political changes and things like that. How do we view potential impacts to those sectors specifically coming from this election? And obviously technology, healthcare, big U.S. sectors, but energy very important to Canada as well. So any thoughts there? And Brooke, we’ll start with you there.

Brooke Thackray: Yeah, well, so this comes back to Anu’s point on the dispersion. I mean that’s the whole thing is you’re going to see a lot of betting on sectors coming up very shortly. In fact, I saw BOA [Bank of America] piece just recently talking about if Harris gets in and with the corporate tax rate increasing it from 21% to 28%, that’s going to end up with a 5% hit to the earnings per share on companies. And that’s quite a bit, but then you start going through the different sectors, which is really important. So the consumer staples, consumer discretionary would be the hardest hit and technology would be at the bottom. So you’re going to see a lot more reporting as far as the different sectors of the market go. And if you take a look, I got another slide here as well on this, and this is the sector performance and I through the Russell 2000 at the end.

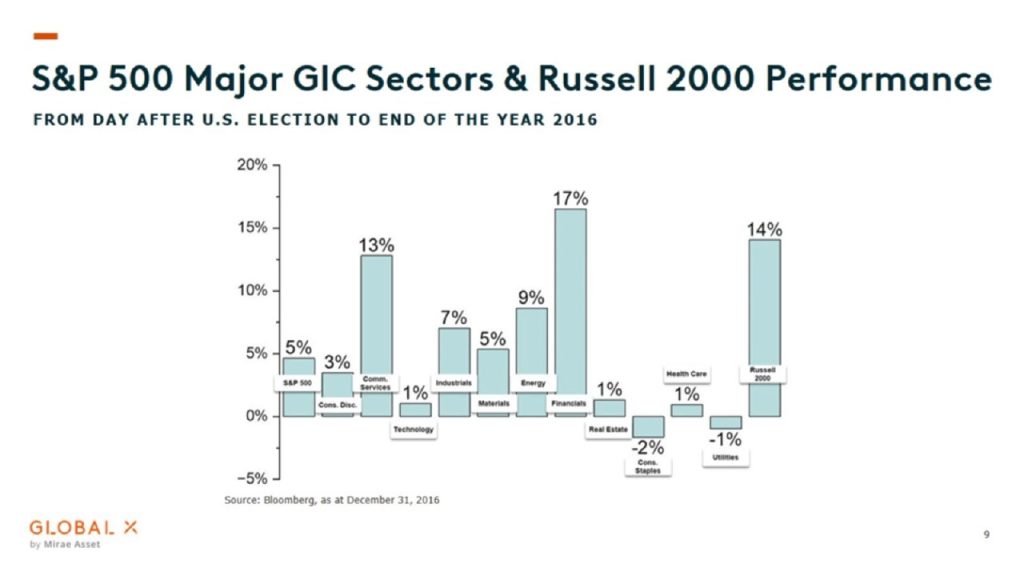

So this is the major gig sectors here we are for the S&P sectors and the Russell 2000 at the end, this is after Trump was elected. So the day after the end of the year, a couple of things. Financials did really well, different time back then, totally different time as far as that goes. So it’s really because of strong economic growth anticipation, that’s really what took place there. Small caps really rocketed higher as well and did extremely well. One because they’re heavily weighted as far as constituency factors to financials, but also because of his domestic policies. I think if Trump did get in, I think if we start parsing out which sectors would do better under which candidate, I think that the small cap sector would probably, it’s a Trump trade basically would probably do better. So if you start to see him increase odds and polls of actually winning, I think you’ll see the small caps actually pick up in relative performance. Interestingly enough, look at technology, it was only 1% up from the election and that could be totally different this time around because we’ve got totally different circumstances taking place here as far as that goes. So I think that you’d probably see a lot more technology in play.

I think Trump would probably benefit more with the technology side just because of the tariffs that he’s proposing. There are other negative impacts with tariffs and everything else, but the technology sector would probably benefit from that as well. Energy sector between them, I think Trump would probably end up better with those industrials and some of the cyclicals could actually be better under Harris. And the reason for that is just because of the spend that they would do on that side of things. So overall there’s a different mix of who gets in as far as that goes and that’s why we get that large dispersion in sectors and it’s going to happen very fast one way or the other. And that’s the whole thing. This isn’t something you can take a look at and go, oh, I think that I’m going to go into small caps, small caps have that huge rocket higher, but they peaked at the end of December, actually January 3rd or something and fell off. So just that excitement trait taking place. But there are differences between the two candidates in which sectors are going to benefit. And I think you sort of have to go through and take a look and say which sectors, what are the variables affecting the different sectors on that?

Warren Lovely: And just picking up from some of the earlier cautions I think as well you need to control for the fact, well how easily will these proposed plans get implemented? And a lot of that’s going to come down to what’s the extent of congressional control that the president’s party enjoys, how much can be done through executive order or through agencies and other sort of backdoor channels and so on. There is a scenario where the winning party holds both houses of Congress and we’ve seen in the past that in those instances you can have a really impactful two-year period until you get to the midterms where you can really push through and make progress on your agenda without running into that sort of congressional dysfunction or a gridlock that characterizes oftentimes the back half of a mandate. So I think again, if I could just repeat the caution a lot to control for here and clearly in terms of the individual’s sector performance, you can be looking at each candidate’s individual pledges.

I think in some cases there’s less division, less divisiveness on energy policy now than I think in the past on tech. I think what’s also clear, Brooke, you probably would tend to agree with this, we’ve [00:31:30] gone through a technological revolution and we’re in the midst of one now versus 2016. So again, you got to be careful about drawing too many conclusions. I think Chris, if I’m not mistaken, there was a part of this question as well that related to how does the falling or the interest rate backdrop factor into your thinking here on this? The one thing I would just say on this, and without repeating too gloomy a message, I would say that there’s the great hope of course, that these lower interest rates that we know are coming, right? The Fed’s going to cut interest rates next week, 25 basis points…

Brooke Thackray: You heard it here.

Warren Lovely: …and continue on a path to lower interest rates and that’s going to reignite economic growth and save the day in effect. And obviously on interest rate sensitive sectors, that’s a big consideration. I would just say be mindful of the fact that the reason why interest rates are falling is really twofold. One, we’ve secured price stability, price almost there in the U.S. context we’re there in Canada, but more than anything we have now with inflation relatively well under control, the Fed is pivoting to that other part of its mandate, the labour market. And as I said before, developments there are problematic and as a result it generally leaves me notwithstanding the election, a little bit more defensive on a sector basis. I’m not sure.

Anu Ganti: And just one point you mentioned revolution, technology revolution. I think that goes to the point you’ve heard so much about sectors, you’ve heard so much about history. These things aren’t static, right? They’re not the same sectors they were in the nineties or in the eighties or in the seventies. We’ve done some or eight years ago, exactly. Even eight years ago in the nineties, late nineties. If you think back to the tech bubble, the tech companies of today are a lot stronger, more robust from a quality perspective than they were a couple of decades ago. So keep in mind that these things, shift over time.

Chris McHaney: Yeah, lots of cash being generated by those tech giants these days.

Brooke Thackray: Chris, you had one there for, I think on the question it was talking about the Canadian sectors as well. I think that was part of that there on the…

Chris McHaney: Slide. Yeah, in particular, I mean I mentioned energy, but…

Brooke Thackray: No, I was just going to say as far as Canada goes, as far as the election in the States goes, we will be impacted by this. I mean there are tariffs in place and if you take a look at something like the Softwood lumber treaty, I mean we’ve had problems for decades on that. I mean the rules are the rules, but the U.S. tends to break the rules at their own will.

Warren Lovely: Under both parties?

Brooke Thackray: Yes, both parties, absolutely. I mean, well decades it’s been going on and it’s still going on. I can’t believe this. And I think today’s relationships with countries around the world is that look what’s happening with the tariffs that the U.S. and Canada proposing are in place of putting ’em in place. I mean these aren’t because of dumping going on, they’re just putting them on some things. They’re just saying we’re just going to do it. And so this is the new era that we’re in right now and I think Canada will be affected by that largely as well. Some sectors maybe not so much, but I think the manufacturing sector in Canada is going to, will be impacted and I think it’s going to be both parties. If I had to say which party would probably have the most detrimental effect, it would probably be the Republicans jU.S.t based upon previous, when Trump was in power in 2016 where they’re just going to guard their borders as far as product goes, going back and forth. So I think some of the cyclicals as far as metals and whatnot could affect it. But definitely the manufacturing.

Warren Lovely: Yeah, this is an important cautionary note. We’re basically taking decades of progress on globalization and trade liberalization and turning it on its head, turning it back, and this de-globalization process is not unique to the U.S. I mean we’re participating in it as well here in Canada. I think there’s a couple of important implications there. One, and we’ve heard central bankers warn on this, we had the Bank of Canada Governor just on Tuesday, in fact reminding U.S. of the perils of deglobalization, it’s inflationary. So I realized I’ve proposed a cyclical story here that gets U.S. to lower interest rates because the economy really is weakening, but you do worry about this beggar, thy neighbour, trade policy, deglobalization, protectionism, tariffs and so on. Maybe jU.S.t structurally embedding more inflation in the economy and maybe as a result, not getting U.S. to as easy and interest rate policy as we would have otherwise.

Brooke Thackray: Or making U.S. more susceptible to another wave of inflation, which could happen as well down the road.

Chris McHaney: I would say even a neutral rate of neutral interest rate is probably a lot higher than what a lot of people are even used to given the last 10, 15 years would.

Warren Lovely: Yeah, you said it better than I did. Yeah.

Chris McHaney: We’ll zoom out just a little bit here. More higher, greater picture. And Warren, maybe I know your answer to this one already given some of your comments, but historically, Canada Canadian investors have had one of the largest home biases in their portfolios globally, but of course the U.S. over the last call it 10 plus years has been a global driver of markets. Does it make sense to revisit allocations for Canadians, whether that be reducing that Canadian home bias, whether that be taking profits from the U.S. and going elsewhere and diversifying, maybe Anu, you can take that off.

Anu Ganti: This is such an important topic, right? Thinking about home bias, and we’re sitting here in Toronto and what I’ll do is I’ll give you a couple of index stats to kind of set the stage. If you look at our S&P Global BMI index, the U.S. weight is 62%, roughly. Canada’s weight is roughly 3% pause there, right? Big difference right now coming back to sectors, huge differences when you look at the S&P 500 versus, say the S&P TSX-60 or the TSX Composite. If you look at the S&P 500, of course dominated by information, technology, financials, healthcare. If you look at the TSX 60 financials, energy industrial materials that composites weight in information technology from memory was only 8%, right? So very difficult to ignore the U.S. when you’re thinking about technology. With all the discussion we’ve talked about with the revolution in technology.

So important to think about these things as compliments when looking at sectors, when looking at more granular industries. One other point is we talked a lot about sectors and home bias and country biases. Coming back to the points on mid and small caps, some of our research has shown historically that Canadians have tended to be underweight within the mid- and small-cap space when looking at the cap spectrum. And there can be a number of reasons for this, perhaps smaller caps for more expensive trade. Our SPIVA scorecards that we produce show that it’s tough to beat the benchmark even within the smaller cap space. So there could be a number of reasons. So important I think to look under the hood at the sector exposures and look at what kind of cap exposure you’re getting as well.

Brooke Thackray: I think this is a very interesting question because we’ve seen the U.S. seven stocks, et cetera, blah, blah, blah, perform and really skew the whole market. And it’s frustrating because we do have that home bias in Canada. I mean in people do pick up some U.S. stocks. I mean the good news for Canadians investing, I think somebody might have some stats on this, is we do have a large home bias, but outside of our home bias, we tend to favour the U.S. versus. the rest of the world. So that’s actually being a benefit. I think I knew agree with me on that, but that could change down the road. Let’s just go back to 2000 for a second. I talked about that earlier when the technology bubble did burst and down the other side of the mountain there is when the stock market corrected for the next six years, Canada was right up there.

I mean, we outperformed the S&P 500 for a number of years. So yes, we have this home bias, and I totally agree with Anu. We have to go out into different areas of the market and different areas of the world, but coincidentally, we actually could actually do quite well over if we go back into a commodity supercycle, if all of a sudden now we’re short oil, we’re short copper, we’re short gold, we’re short, silver uranium, you name a list, but just nobody cares. This is exactly like it was back in 2000 and that will change. And so the home bias might accidentally actually be not such a bad thing down the road, but I still think you can’t count on that and you still have to have the optimal portfolio as far as that goes, but we could actually see candidates actually do quite well. I’m not saying that’s going to happen now in 2025 or whatever, but maybe that takes place coming up after that 2026 and up to 2030 and when the market narrative changes and it will change at some point. I think we’re

Warren Lovely: Getting pretty short of time. I’ll just say on this very, very quickly, that international exposure needs to be, I think, more thoughtful these days. Again, what we’re talking about here is a process of maybe decoupling in terms of traditional economic relationships. So placing investments blindly and either advanced markets offshore or emerging markets. I think it needs to be done a little bit more thoughtfully, selectively these days. So maybe it’s a North American bias.

Brooke Thackray: Oh, there is a North American bias. Absolutely. And if you compare portfolios to 20, 30 years ago, I mean Europe was included more and emerging markets. I mean, okay, if you’ve invested in emerging markets recently, not so good, but that’s going to change if the U.S. dollar does [00:41:30] go down and we become more commodity focused. Emerging markets, they’ve changed their nature, but will still do well. So things I think will change over time.

Anu Ganti: I think part of that is just different ways to gain your exposure that say, 50 years ago, how did I get my exposure? Now there’s so many options through an index, through derivatives, so forth.

Chris McHaney: Great. Okay, I think we’re at time, so I want to thank again everyone for joining us today. Thank you to the panel for your great insights.

Topics: Covered Calls

Not ready to invest, but curious to learn more?

Subscribe for research perspectives, market commentary, and charts of the trends shaping global markets. We promise not to overwhelm you – updates will be periodic and timely.