As the number of Artificial Intelligence (AI) initiatives grows, so have the power demands of hyperscalers and global data centres. By 2026, these global hubs are projected to consume as much energy as the entire country of Japan, underscoring an urgent need for long-term energy solutions.1 Nuclear energy may be poised to play a pivotal role. The uranium market, essential for nuclear fuel, is already facing supply constraints, creating a challenge for suppliers and buyers alike. Global public policy, particularly recent U.S. policies, may lighten the burden further for nuclear reactor construction.

Key Takeaways

- With a track record of power reliability, nuclear energy is increasingly seen as the optimal solution to meet the massive energy demands of expanding artificial intelligence technologies.

- The nuclear industry is already grappling with supply and demand challenges. Geopolitical factors driving renewed demand from utilities may further exacerbate these issues.

- In the U.S., nuclear energy has garnered bipartisan support, with recent laws aimed at expanding the nuclear capacity of the world’s largest reactor fleet.

AI’s Power Needs Present a Significant Challenge

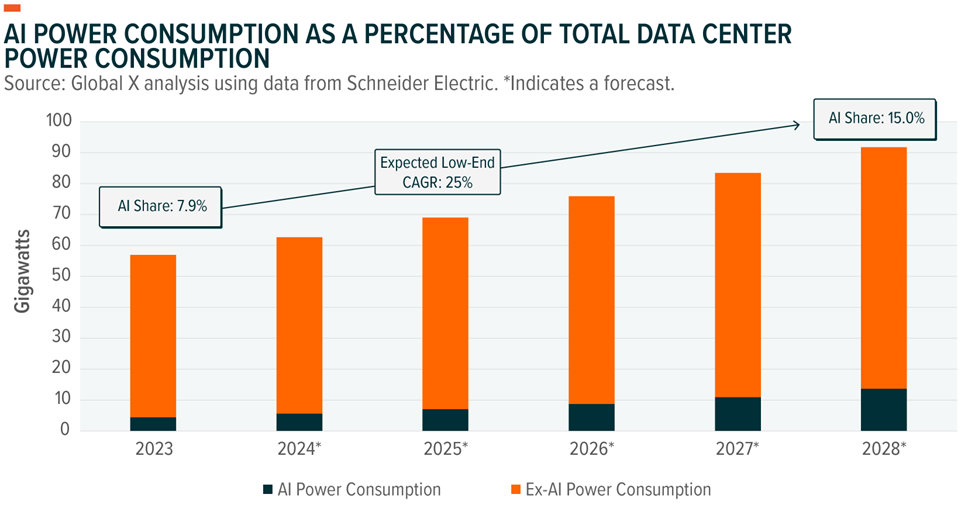

AI’s growing presence in data centres is increasing rack power densities, requiring AI start-ups, enterprises, colocation providers, and internet giants to adapt their data centre design and management.2 U.S. power demand is projected to grow at a 2.4% compound annual growth rate (CAGR) through to 2030, compared to approximately 0% over the last decade.3 Data centres are expected to account for 0.9 percentage points of this growth.4 The percentage of AI’s power consumption as a percentage of total data centre power is expected to grow from 8% to a potential range of 15-20% by 2030, representing a CAGR of 25-33%.5 These expected energy needs are unprecedented, and hyperscalers are expected to spend $200 billion in capital expenditures in 2024 alone to meet AI and climate goals simultaneously.6

The reliability of nuclear reactors as a clean energy source is already being leveraged. With capacity factors (a measurement of reliability) exceeding 90%, nuclear energy is positioned prominently in the AI infrastructure discussion since data centres operate nearly 24/7.7

Hyperscalers, data centre owners, and utilities alike have taken steps to address these mounting issues. Talen Energy sold a 1,200-acre campus to Amazon Web Services (AWS) for $650 million, powered by a 2.5 gigawatt nuclear plant.8 Amazon also recently filed for a data centre campus in Louisa County, Virginia, adjacent to the North Anna Nuclear Power Station.9 Constellation Energy agreed to supply up to 35% of the energy for Microsoft’s Boydton, Virginia, data centre from nuclear power.10 All the while, Equinix became the first major colocation data centre REIT to enter a small modular nuclear reactor (SMR) deal in a move towards integrating nuclear power, signing a pre-agreement with Oklo for up to 500 megawatts (MW) of nuclear energy.11

Uranium Needs for AI & Data Centre Solutions May Exacerbate an Already Existing Deficit

Uranium miners are a critical component in the nuclear supply chain, given the significance of triuranium octoxide (U3O8) as the key fuel source needed for nuclear reactors. The war in Ukraine led to a major shift in Western nations’ nuclear policy, as Europe and the U.S. aimed to diversify their energy sources while reducing their dependence on Russian natural resources. As a result, the pace of global reactor shutdowns has slowed, and the construction of new nuclear power plants has increased.12,13 Citing public and private sector shifts, utilities companies expect different sources of renewable energy will be sought after with nuclear as a key solution.14 Uranium miners may be able to take advantage of growing demand that could offer greater pricing power and elevated U3O8 prices.

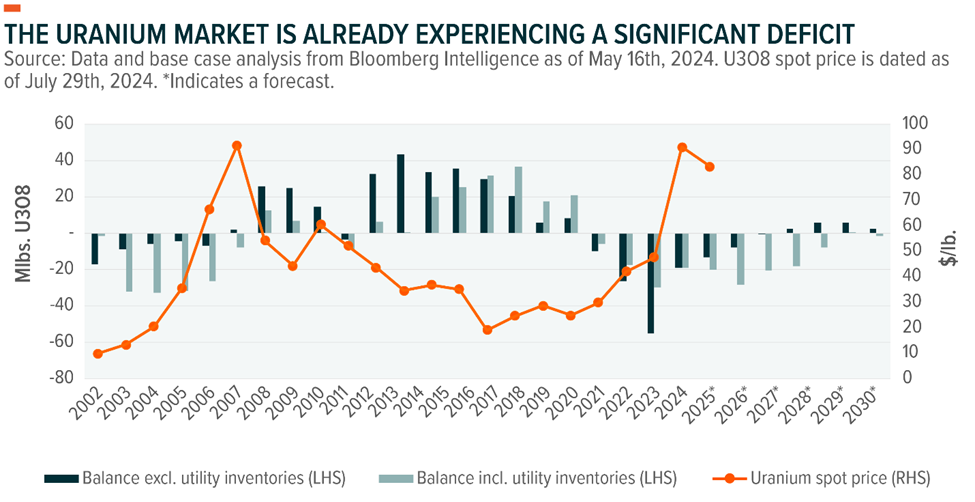

The graph below demonstrates the supply and demand balance of the uranium market with and without utility inventories. Assuming utility restocking ramps up over the next few years, it may take until 2029 for the market to reach equilibrium again.

Production is expected to be primarily driven by Canadian, U.S., and Australian companies.15 Expanding production within existing mines may be a cost- and time-effective solution. During its second-quarter 2024 earnings report, Cameco reaffirmed its announcement to extend the Cigar Lake mine’s life to 2036.16 It also continues to anticipate production to expand at McArthur River/Key Lake from 18 million pounds to 25 million pounds.17 Meanwhile, Kazatomprom, the world’s largest uranium producer, recently increased its 2024 production guidance by 6% from the first to the second quarter of 2024.18 Junior and senior uranium miner exploratory partnerships paired with continued regulatory overhauls to tap into existing reserves will be key and necessary solutions in the long term.19,20

The pent-up demand for nuclear energy seems to be a global phenomenon. During the 28th United Nations Conference of Parties (COP), 25 nations announced their ambition to triple nuclear capacity by 2050.21 Achieving this goal will require significant policy reform, financial innovation, and stepped-up construction. Mainland China is expected to lead the way, with nuclear power potentially becoming 10% of the nation’s total electricity generation by 2035.22 France anticipates building six new reactors by 2035, while Japan recently announced a goal for nuclear to encompass 22% of the country’s power mix by 2030, up from 9% in 2023.23,24 The U.S. is getting in on the action as well.

U.S. Nuclear Capacity and Advancement is Largely a Bipartisan Topic

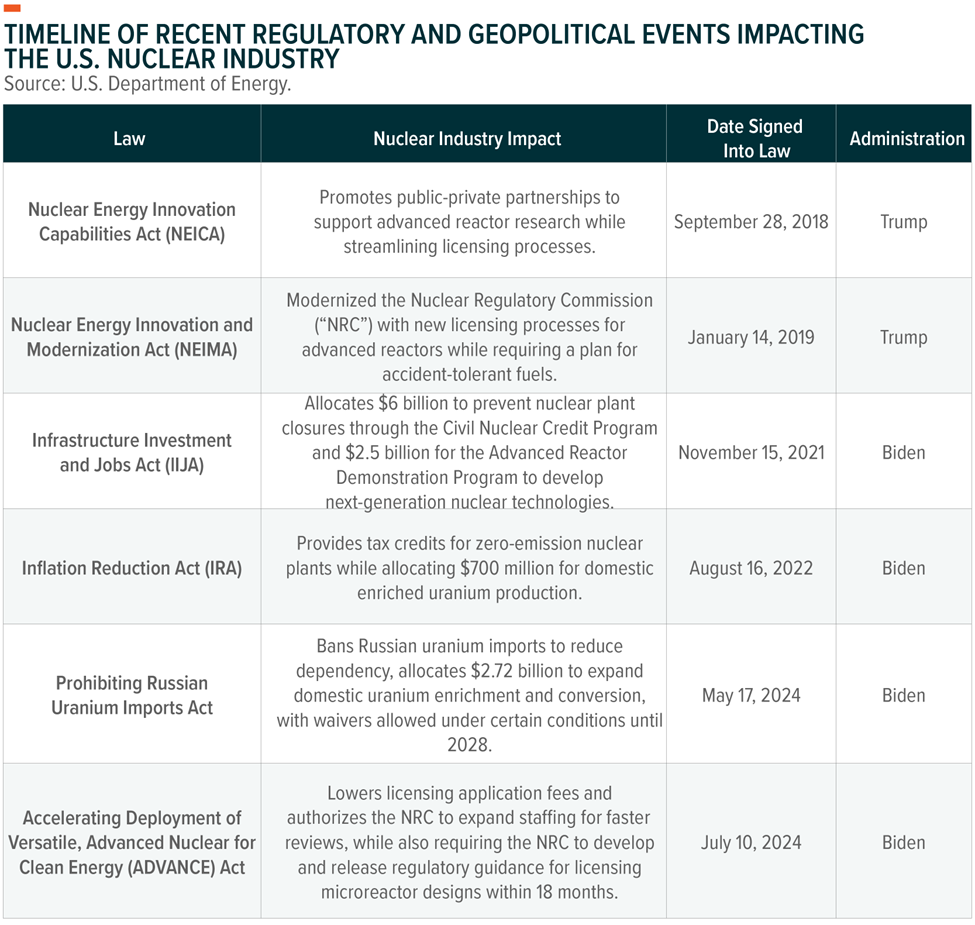

The U.S. currently operates the largest fleet of commercial-use nuclear reactors but has no new nuclear reactors under construction.24 Policies passed over the last few years aimed to reverse this by streamlining processes and lowering the barriers to entry for new technologies, such as small modular reactors (SMRs). This has been a bipartisan issue, and most of the recently passed packages that impacted the nuclear energy industry were passed by either a voice vote or close to unanimous consent.25,26,27,28,29,30

The war in Ukraine has promulgated a strategic shift in U.S. nuclear energy policy. The U.S. is effectively cutting out Russia as its main source of unirradiated low-enriched uranium (LEU) by 2028 (35% of the U.S.’s total imports) through the Prohibiting Russian Uranium Imports Act while unlocking $2.7 billion in new congressional appropriations.31,32 The recently passed Accelerated Deployment of Versatile, Advanced Nuclear for Clean Energy (ADVANCE) Act, signed into law by President Biden, builds off the previous laws enacted during the Trump Administration. This law is intended to increase competition and reduce certain licensing application fees while authorizing increased staffing to expedite administrative processes to shorten the reactor deployment timeframe. Uranium producers with conversion capabilities, uranium enrichment companies, and reactor component manufacturers are likely beneficiaries.

Conclusion: Uranium Producer and Component Equities Have an Enticing Set Up

The uranium market is already facing a significant deficit while being presented with new tailwinds brought about by advancements in artificial intelligence technology alongside global public policy decisions. The U.S. has recently been aggressive in passing new laws aimed at revitalizing its nuclear energy industry while bringing about innovations that could usher in a new phase of nuclear energy production. U3O8 spot markets may be pricing in some of this expected demand, and uranium miners seem to be taking notice. With low-end correlations to both global equities (0.54) and the broader commodities markets (0.42), uranium miners and nuclear component producers offer intriguing, potential portfolio diversification benefits in a market poised for growth.33

Related ETF

FOOTNOTES

1. Wodecki, Ben. (2024, June 04). AI workloads to double data centre power demand by 2026.

2. Avelar, V., Donovan, P., Lin, P., Torell, W., & Torres Arango, M. A. (2023). The AI disruption: Challenges and guidance for data centre design (White Paper No. 110, Version 2.1).

3. Goldman Sachs. (2024, April 28). Generational Growth: AI, data centres and the coming US power demand surge. Goldman Sachs Global Investment Research.

4. Ibid.

5. Avelar, V., Donovan, P., Lin, P., Torell, W., & Torres Arango, M. A. (2023). The AI disruption: Challenges and guidance for data centre design (White Paper No. 110, Version 2.1).

6. Dessai, Tejas. (2024, July 04). Advancing AI requires major data centre and digital infrastructure upgrades.

7. U.S. Energy Information Administration. (2023). Levelized costs of new generation resources in the Annual Energy Outlook 2023. U.S. Department of Energy.

8. American Nuclear Society. (2024, March 7). Amazon buys nuclear-powered data centre from Talen.

9. Purcell, T. (n.d). Amazon provides details for Lake Anna Tech Campus. Lake Anna Life.

10. Judge, P. (2023, June 30). Microsoft signs 24/7 nuclear power deal with Constellation for Boydton data centre. Data Centre Dynamics.

11. Miller, R. (2023, July 25). Equinix puts down $25M in data centre nuclear power deal with Sam Altman’s Oklo. Data Centre Frontier.

12. Statista. (2024). Number of permanent shutdowns of nuclear reactors worldwide from 2005 to June 2024.

13. World Nuclear Association. (2024, July 29). Plans for new reactors worldwide.

14. Kimball, Spencer (2024, June 27). Failure to meet surging energy demand will jeopardize economic growth, utility execs warn.

15. Crofts, M., Balchunas, E., Dougherty, B., & Gadomski, C. (2024). Uranium global industry outlook: Extended market deficit adds price support (Bloomberg Intelligence Deep Dive Report). Bloomberg Finance L.P.

16. Cameco Corporation. (2024). Management’s Discussion and Analysis: Second Quarter (Report No. CCO-2024-Q2-MDA-FS-Notes).

17. Ibid.

18. World Nuclear News. (2024, August 1). Cameco, Kazatomprom release half-year results. World Nuclear News.

19. Junior Mining Network. (2024, August 6). CanAlaska Uranium plans aggressive 2024 exploration programs. Junior Mining Network.

20. BloombergNEF. (2024). Australia’s nuclear-powered distraction threatens net zero.

21. International Atomic Energy Agency. (2023, December 6). Nuclear power finally has its moment at UN climate summit. IAEA.

22. Xin, Z. (2023, September 26). China’s nuclear power to generate 10% of total electricity by 2035.

23. Obayashi, Yuka and Golubkova, Katya. (2024, June 4). Japan’s energy security fears put nuclear back in favour 2040 plan. Reuters.

24. World Nuclear Association. (2024, May 21). Nuclear power in France. World Nuclear Association.

25. Congress.gov. (2017). Actions – S.97 – 115th Congress (2017-2018): An act to enable civilian research and development of advanced nuclear energy technologies by private and public institutions, to expand theoretical and practical knowledge of nuclear physics, chemistry, and materials science, and for other purposes. Library of Congress.

26. Congress.gov. (2018). Actions – S.512 – 115th Congress (2017-2018): An act to modernize the regulation of nuclear energy. Library of Congress.

27. Congress.gov. (2021). Actions – H.R.3684 – 117th Congress (2021-2022): Infrastructure Investment and Jobs Act. Library of Congress.

28. Congress.gov. (2022). Actions – H.R.5376 – 117th Congress (2021-2022): Inflation Reduction Act of 2022. Library of Congress.

29. Congress.gov. (2024). All Info – H.R.1042 – 118th Congress (2023-2024): Prohibiting Russian Uranium Imports Act. Library of Congress.

30. U.S. Senate Committee on Environment and Public Works. (2024, July 9). Signed: Bipartisan ADVANCE Act to boost nuclear energy now law. U.S. Senate Committee on Environment and Public Works.

31. Miller, Matt. (2024 May, 14). Prohibiting imports of uranium products from the Russian Federation. U.S. Department of State.

32. U.S. Department of Energy. (2024, July). Russian uranium ban will speed development of U.S. nuclear fuel supply chain. U.S. Department of Energy.

33. Global X analysis with data from Morningstar Direct, measured using monthly returns from August 1st, 2019 to July 31st, 2024.

GLOSSARY

Triuranium Octoxide: A compound of uranium, represented by the chemical formula U3O8. It is one of the most stable forms of uranium oxide and is a key material in the nuclear fuel cycle.

Correlation: A statistical measure that describes the extent to which two variables are linearly related. It indicates the strength and direction of a linear relationship between two variables and ranges anywhere from -1 to 1.

DISCLAIMER

Commissions, management fees, and expenses all may be associated with an investment in products (the “Global X Funds”) managed by Global X Investments Canada Inc. The Global X Funds are not guaranteed, their values change frequently and past performance may not be repeated. Certain Global X Funds may have exposure to leveraged investment techniques that magnify gains and losses which may result in greater volatility in value and could be subject to aggressive investment risk and price volatility risk. Such risks are described in the prospectus. The prospectus contains important detailed information about the Global X Funds. Please read the relevant prospectus before investing.

Certain ETFs are alternative investment funds (“Alternative ETFs”) within the meaning of the National Instrument 81-102 Investment Funds (“NI 81-102”) and are permitted to use strategies generally prohibited by conventional mutual funds, such as the ability to invest more than 10% of their net asset value in securities of a single issuer, the ability to borrow cash, to short sell beyond the limits prescribed for conventional mutual funds and to employ leverage of up to 300% of net asset value. While these strategies will only be used in accordance with the investment objectives and strategies of the Alternative ETFs, during certain market conditions they may accelerate the risk that an investment in ETF Shares of such Alternative ETF decreases in value. The Alternative ETFs will comply with all requirements of NI 81-102, as such requirements may be modified by exemptive relief obtained on behalf of the ETF.

Certain statements may constitute a forward-looking statement, including those identified by the expression “expect” and similar expressions (including grammatical variations thereof). The forward-looking statements are not historical facts but reflect the author’s current expectations regarding future results or events. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. These and other factors should be considered carefully and readers should not place undue reliance on such forward-looking statements. These forward-looking statements are made as of the date hereof and the authors do not undertake to update any forward-looking statement that is contained herein, whether as a result of new information, future events or otherwise, unless required by applicable law.

This communication is intended for informational purposes only and does not constitute an offer to sell or the solicitation of an offer to purchase investment products (the “Global X Funds”) managed by Global X Investments Canada Inc. and is not, and should not be construed as, investment, tax, legal or accounting advice, and should not be relied upon in that regard. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. These investments may not be suitable to the circumstances of an investor.

All comments, opinions and views expressed are generally based on information available as of the date of publication and should not be considered as advice to purchase or to sell mentioned securities. Before making any investment decision, please consult your investment advisor or advisors.

Global X Investments Canada Inc. (“Global X”) is a wholly owned subsidiary of Mirae Asset Global Investments Co., Ltd. (“Mirae Asset”), the Korea-based asset management entity of Mirae Asset Financial Group. Global X is a corporation existing under the laws of Canada and is the manager, investment manager and trustee of the Global X Funds.

Published August 23, 2024

Categories: Articles, Insights

Topics: A.I., Commodities, Uranium