Authored by Global X Research Team

The MSCI Emerging Markets Index has only outperformed the S&P 500 Index in two out of the last 11 calendar years through 2023.1 However, during the last emerging market (EM) cyclical upswing, between 2001 and 2010, the MSCI Emerging Markets Index delivered a cumulative return of 344.40% versus 15.07% for the S&P 500 Index.2 This poses the question if EM equities could be at the precipice of a new cyclical upswing. Though we’ll refrain from making an outright call on the collection of 26 different countries, economies, and political systems classified as “emerging markets,” we do point to a few different positive indicators.

Where Are We?

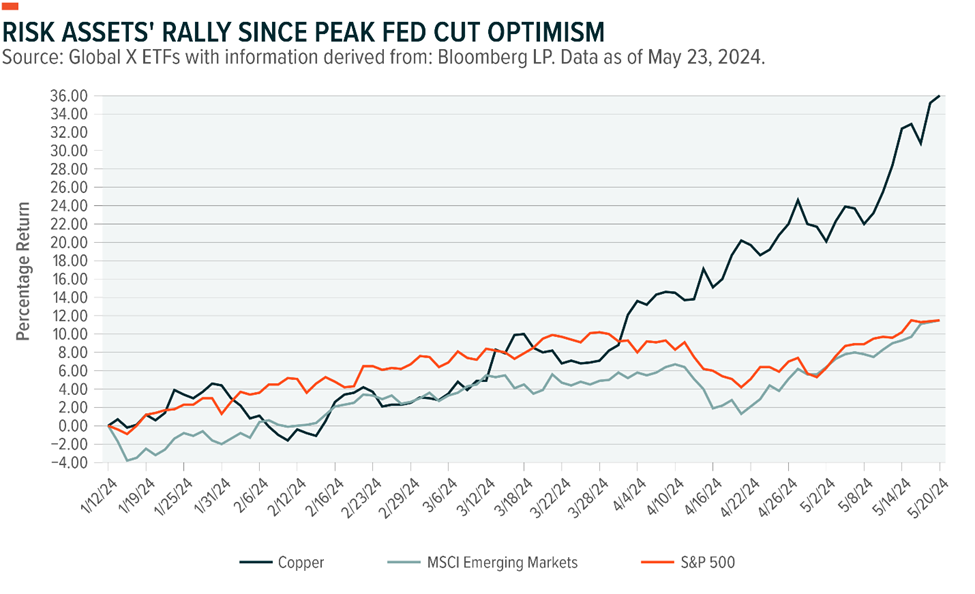

- Demand: The market reached peak U.S. Federal Reserve (Fed) interest-rate cut rhetoric in January 2024. Despite incremental hawkish language, higher yields, and a stronger U.S. dollar (USD) since then, copper, gold, oil, and EM assets have counterintuitively rallied. To us, this signals that the markets are moving based on structural supply and demand factors, expansionary Purchasing Managers’ Index (PMI) numbers, and a pickup in capital expenditure (capex) cycles – not simply interest rate speculation. If/when the U.S. Federal Reserve (Fed) does begin cutting interest rates, this could add fuel to the fire. We note that the JPMorgan Global Manufacturing PMI Index has been above 50 for every month this year and on a rising trend through May (after being in contractionary territory for 16 straight months, and still well below the previous cycle peak of 55.5 in June 2021).3

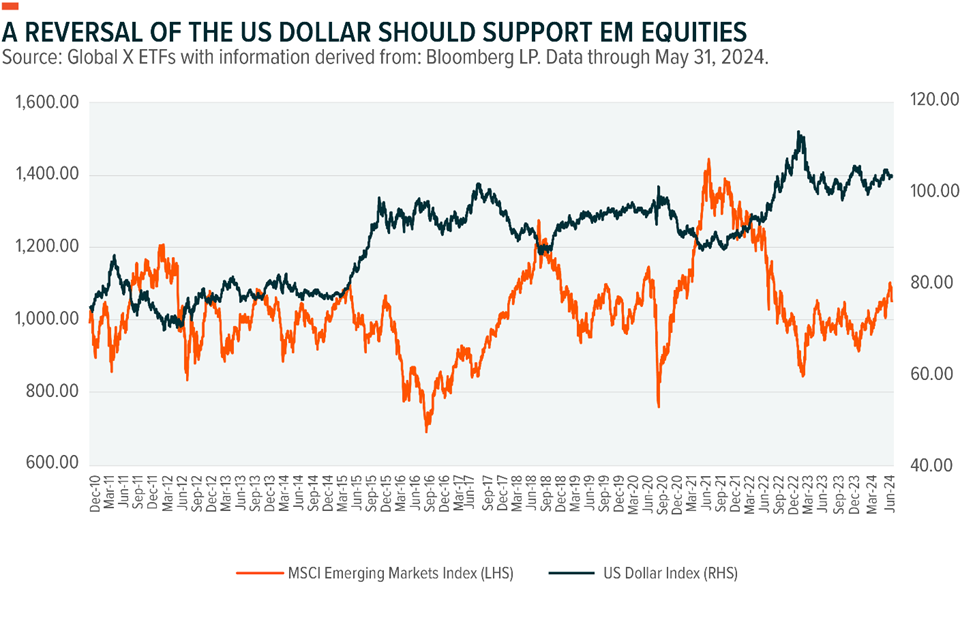

- The Dollar: We see the U.S. dollar as the most impactful driver of broad emerging market equity performance. Historically, EM equities as measured by the MSCI Emerging Markets Index have displayed an inverse relationship with the dollar (gaining roughly 4% for every 1% downward move of the USD).4 This correlation is due to both:

- The inverse relationship between USD and commodity prices, and

- EM countries and the companies within them having historically funded their growth with USD debt.

When establishing a view on the U.S. dollar, it is important to consider the following factors:

- The Fed has signaled a potential end to its monetary policy hiking cycle. Lower rates, inherently, attract less capital, which means less demand for U.S. dollars and, hence, potential weakness.

- An uncertain and polarizing presidential election cycle in which both leading candidates have displayed a propensity to spend and increase the U.S. fiscal deficit.

- Diminishing confidence in key institutions, as “looming” government shutdowns have become common practice.

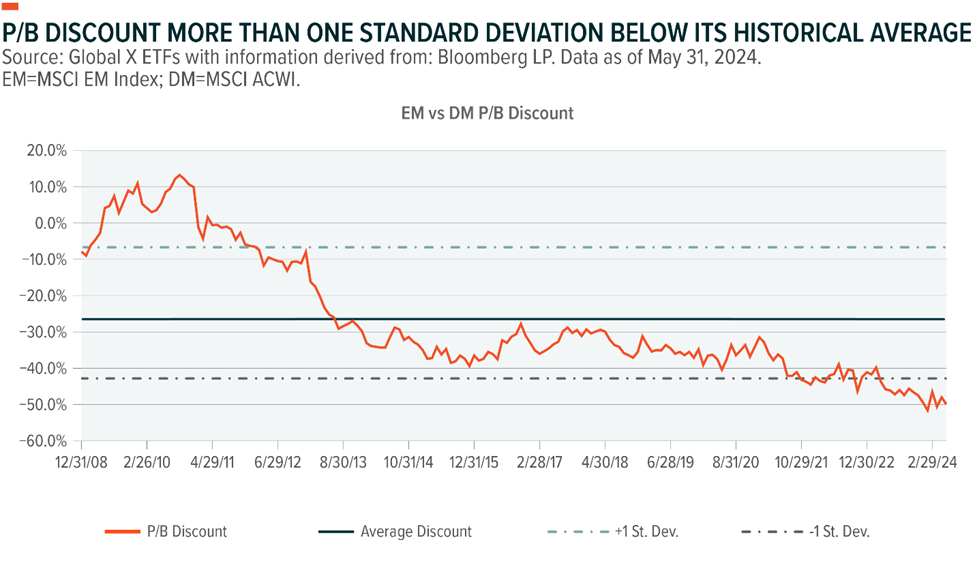

- Valuations: Despite higher gross domestic product (GDP) growth, EM equities trade more than one standard deviation below their historical average discount to developed market equities.5 Broad EM equities trade at 11.18x earnings versus 19.42x for the S&P 500 Index with double the dividend yield and higher expected growth rates.6 A lower standard deviation indicates lower volatility. The Price-to-Book (P/B) ratio is a measure of a listed company’s market capitalization to its book value (the net value of a company’s assets as reflected by its balance sheet). Investors typically use P/B ratios to find undervalued companies.

Looking Forward

We have noticed a significant pickup in interest in emerging markets. Many investors are coming from low to no exposure to this asset class and are looking for differentiated ways to find outsized growth at discounted valuations. Some are in search of a U.S. dollar hedge, many are looking for alpha potential, and others are simply looking for diversification. We see various opportunities within the asset class but are most excited about India from a long-term structural perspective; Brazil on the verge of a potential 6–12-month cyclical upswing; Argentina as a high-risk/reward turnaround; and Greece as a way to unlock deep value. In China, we are neutral with limited visibility on the whole market but see a bright spot within domestic consumption.

- Asia: We began the year with a call to “be greedy when others are fearful” in our 2024 China outlook and now remain selectively optimistic on segments of China’s equity market – specifically within Chinese consumption. Broadly speaking, a combination of a low earnings base, economic normalization, and continued stimulus could drive positive earnings per share (EPS) revisions. However, we also see headwinds in the country. The U.S. election cycle could bring increased hawkish rhetoric on China’s trade and military operations, and we also see regulatory uncertainty around specific sectors, which could keep investors at bay. From a valuation perspective, after the year-to-date rally, the broad MSCI China Index trades in line with five-year historical averages.7 That said, we believe China’s consumer sector stands out as a unique opportunity. We continue to see India as the best long-term structural story in emerging markets and still see opportunities for positive earnings revisions. Southeast Asia and Vietnam also look attractive from a structural perspective. On the cyclical side, we see opportunities for companies in Taiwan and Korea to continue to benefit from the surge in demand for semiconductors, but we are wary of political headwinds, trade rhetoric, and an eventual slowdown in U.S. demand.

- Latin America: Latin America offers a diverse set of economies with outsized exposure to commodities trading at low valuations. Brazilian equities came under pressure in the first half of the year but, looking ahead, we see room for optimism. We see further room for the Central Bank (COPOM) to continue its monetary policy easing cycle, with lower interest rates likely driving flows from local fixed income markets into equities, reducing floating rate borrowing costs, and spurring credit growth. Beyond these short-term drivers, Brazil remains a commodity powerhouse, exporting oil, gas, iron ore, soy, proteins, and other products around the world. Though Mexico still benefits from positive real interest rates and “nearshoring” tailwinds, recent elections have brought the Morena party an unprecedented amount of power, increasing the risks for controversial constitutional changes, pressure on the fiscal balance, and economic headwinds. In the Andean region, we expect the elevated copper price environment to remain a tailwind for both Chile and Peru, which produced ~1/3 of global supply in 2022, helping support the currencies and potentially translating into higher levels of consumption.8 Colombia’s political backdrop remains challenged, however, depressed valuations, low investor positioning, and the country’s outsized exposure to oil could extend the market’s recent rally into the second half of the year.

- Emerging Europe, Middle East, & Africa (EEMEA): This broad region offers diverse opportunities for investors. Within Emerging Europe, we are optimistic about the combination of moderating inflation, easing monetary conditions, and lower policy rates potentially supporting an acceleration of growth into the remainder of the year. European Union Recovery and Resilience Facility (RRF) funds are also starting to flow through economies, governments are maintaining consumer-friendly policies, and the European Central Bank (ECB) made its first interest rate cut in June. Within the Middle East, we see long-term themes continuing to develop. In Saudi Arabia, the government will need to balance not only global oil markets to support prices for its growing fiscal needs but also its capex plans for mega projects. Other Gulf Cooperation Council (GCC) peers are also going through powerful reforms as they compete with Saudi Arabia for investment and growth in the region. Importantly, the region has benefited from its U.S. dollar pegs and could, counterintuitively, provide a haven within EM despite broader geopolitical risks. South Africa’s second-half performance looks promising on the back of the recent Africa National Congress and Democratic Alliance (ANC and DA) led coalition in government, which will likely tilt to the center and allow investors to focus on fundamentals. Turkey is expected to maintain economic orthodoxy as the government pursues disinflation, which could support foreign flows and reserve accumulation. Egypt is on a path of macro stabilization, but risks, especially around FX, remain.

Spotlighting Opportunities

- Structural: We believe India is the best structural, long-term, opportunity in the world, driven by a combination of attractive demographics, market-friendly (and democratically elected) governance, supply chain diversification out of China, and a growing middle class – all on top of a unique “digital stack.” Vietnam is another structural story that could benefit from a strong demographic dividend coupled with continued manufacturing diversification out of China.

- Cyclical: We see two unique cyclical opportunities. From a concentrated perspective, we believe Brazil looks especially attractive due to discounted valuations, an advanced monetary policy cycle, and broad exposure to a robust commodity base. From a currency perspective, Brazilian equities have historically delivered roughly 5% returns for every 1% weaker move of the U.S. dollar.9 In a more diversified approach, we believe EM ex-China provides balanced exposure to the commodity and interest rate stories in Latin America & EEMEA along with the artificial intelligence technology surge coming out of North Asia.

- Value: We see Greece and Colombia as unique pockets of deep value in EM. Despite geopolitical neutrality, a market-friendly government, and strong economic momentum, Greece still trades below 1x book value with a 6.93x P/E and solid 6.75% dividend yield.10 All three rating agencies have upgraded Greece’s credit to Investment Grade, and we see an opportunity for a potential upgrade to Developed Market status in the next three years. Greece is forecast to grow nearly 3% this year, well ahead of the euro zone average of 0.8%.11 Colombia trades at depressed multiples of 0.76x book value and 5.70x P/E with an 8.48% dividend yield.12 The market is already pricing in market un-friendly reforms, though we recognize political gridlock and a path back towards the center. Additionally, rising energy prices could provide a powerful tailwind for the economy.

- Contrarian: Argentina and China’s consumer sectors offer two interesting contrarian opportunities within emerging markets. Argentina’s President Milei has made great strides in the first six months of his Presidency in returning Argentina’s economy to orthodoxy, passing key economic reforms, devaluing the currency, and cutting irresponsible fiscal spending. The country is already seeing surpluses in terms of its fiscal and trade balances, and we expect to see continued progress on reforms this year. This momentum could further bolster his support heading into the 2025 mid-term elections. In China, falling home prices, weak global goods demand, and high levels of unemployment have recently weighed on the Chinese consumer and brought down valuation multiples more than one standard deviation below their five-year historical averages.13 However, the sector is unique in its strong alignment with the Chinese Communist Party’s goals to double the middle class and drive domestic-led growth.14 Looking to the second half of the year, Chinese consumer names (which include apparel, technology, autos, travel, and more), look promising based on valuations, government stimulus, and ongoing support for the property sector.

- Thematic: We continue to believe the long-term evolution of EM economies shifting from asset-heavy, low-return exporters to asset-light, profitable, domestic service & goods providers remains intact. History doesn’t repeat, but it often rhymes. The economic backdrop and post-WWII “baby boom” led to a significant expansion of the U.S. middle class. The U.S. benefitted from 76.4 million baby boomers born from 1946 through 1964.15 Global X believes there will be various similar economic patterns across emerging markets, as roughly five billion people are expected to join the consumer class by 2031.16 This megatrend, along with reducing the unknown volatility around FX, commodity prices, and trade rhetoric, increases our optimism around domestic consumption stories across emerging markets.

Related ETFs

Global X MSCI Emerging Markets Index ETF (EMMX.U**/EMMX)

Global X MSCI Emerging Markets Covered Call ETF (EMCC)

Global X Enhanced MSCI Emerging Markets Index ETF (EMML)

Global X Enhanced MSCI Emerging Markets Covered Call ETF (EMCL)

**Trades in U.S. dollars

Sources

1. Bloomberg LP. Data as of December 31, 2023, measured in calendar years.

2. Bloomberg LP. Data from January 1, 2001 through December 31, 2010. Data accessed on April 1, 2024.

3. Bloomberg LP. Data accessed on June 11, 2024.

4. Global X ETFs analysis of data from Bloomberg LP. Data accessed on November 8, 2023.

5. Bloomberg LP. Data as of June 6, 2024.

6. Ibid.

7. Ibid.

8. United States Geological Survey. (2024, Jan). Copper.

9. Global X ETFs analysis of data from Bloomberg LP. January 1, 2003 through December 31, 2023. Data accessed on January 16, 2024.

10. Bloomberg LP. Data as of June 6, 2024.

11. Reuters. (2024, Apr 18). Greek Economy Surges After Decade of Pain.

12. Bloomberg LP. Data as of June 6, 2024.

13. Ibid.

14. South China Morning Post. (2022, Oct 21). China’s ‘Common Prosperity’ Push Could Boost Key Middle-Class, But Action Urged to ‘Bring Back’ Confidence.

15. Population Reference Bureau. (2014, Apr 16). Just How Many Baby Boomers Are There?

16. World Data Lab. (2023, Jul 26). How The World Consumer Class Will Grow From 4 Billion To 5 Billion People By 2031.

DISCLAIMERS

Commissions, management fees, and expenses all may be associated with an investment in products (the “Global X Funds”) managed by Global X Investments Canada Inc. The Global X Funds are not guaranteed, their values change frequently and past performance may not be repeated. Certain Global X Funds may have exposure to leveraged investment techniques that magnify gains and losses which may result in greater volatility in value and could be subject to aggressive investment risk and price volatility risk. Such risks are described in the prospectus. The Global X Money Market Funds are not covered by the Canada Deposit Insurance Corporation, the Federal Deposit Insurance Corporation, or any other government deposit insurer. There can be no assurances that the money market fund will be able to maintain its net asset value per security at a constant amount or that the full amount of your investment in the Funds will be returned to you. Past performance may not be repeated. The prospectus contains important detailed information about the Global X Funds. Please read the relevant prospectus before investing.

Certain ETFs are alternative investment funds (“Alternative ETFs”) within the meaning of the National Instrument 81-102 Investment Funds (“NI 81-102”) and are permitted to use strategies generally prohibited by conventional mutual funds, such as the ability to invest more than 10% of their net asset value in securities of a single issuer, the ability to borrow cash, to short sell beyond the limits prescribed for conventional mutual funds and to employ leverage of up to 300% of net asset value. While these strategies will only be used in accordance with the investment objectives and strategies of the Alternative ETFs, during certain market conditions they may accelerate the risk that an investment in ETF Shares of such Alternative ETF decreases in value. The Alternative ETFs will comply with all requirements of NI 81-102, as such requirements may be modified by exemptive relief obtained on behalf of the ETF.

The funds or securities referred to herein are not sponsored, endorsed, or promoted by MSCI, and MSCI bears no liability with respect to any such funds or securities or any index on which such funds or securities are based. The prospectus contains a more detailed description of the limited relationship MSCI has with Global X Investments Canada Inc. (“Global X”) and any related funds.

Certain statements may constitute a forward-looking statement, including those identified by the expression “expect” and similar expressions (including grammatical variations thereof). The forward-looking statements are not historical facts but reflect the author’s current expectations regarding future results or events. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. These and other factors should be considered carefully and readers should not place undue reliance on such forward-looking statements. These forward-looking statements are made as of the date hereof and the authors do not undertake to update any forward-looking statement that is contained herein, whether as a result of new information, future events or otherwise, unless required by applicable law.

This communication is intended for informational purposes only and does not constitute an offer to sell or the solicitation of an offer to purchase investment products (the “Global X Funds”) managed by Global X Investments Canada Inc. and is not, and should not be construed as, investment, tax, legal or accounting advice, and should not be relied upon in that regard. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. These investments may not be suitable to the circumstances of an investor.

All comments, opinions and views expressed are generally based on information available as of the date of publication and should not be considered as advice to purchase or to sell mentioned securities. Before making any investment decision, please consult your investment advisor or advisors.

Global X Investments Canada Inc. (“Global X”) is a wholly owned subsidiary of Mirae Asset Global Investments Co., Ltd. (“Mirae Asset”), the Korea-based asset management entity of Mirae Asset Financial Group. Global X is a corporation existing under the laws of Canada and is the manager, investment manager and trustee of the Global X Funds.

Published July 8, 2024

Categories: Articles, Insights

Topics: International