Industrial metals markets are experiencing notable shifts, with copper, lithium, and uranium facing supply and demand challenges that could result in an alternative energy and commodities supercycle.

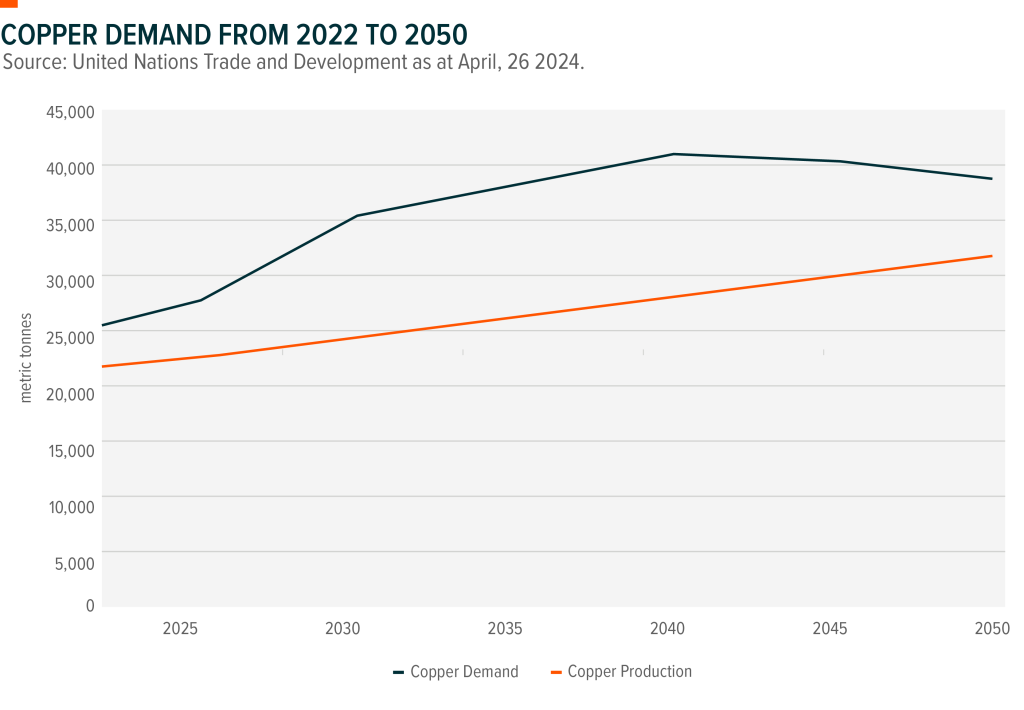

Copper remains crucial for electrification, infrastructure and energy projects, with analysts projecting significant increases in demand over the coming decades as economies and populations worldwide continue to grow. This metal is currently in surplus, but forecasts suggest a potential supply deficit as data centers, electric vehicles, and renewable energy infrastructure expand.

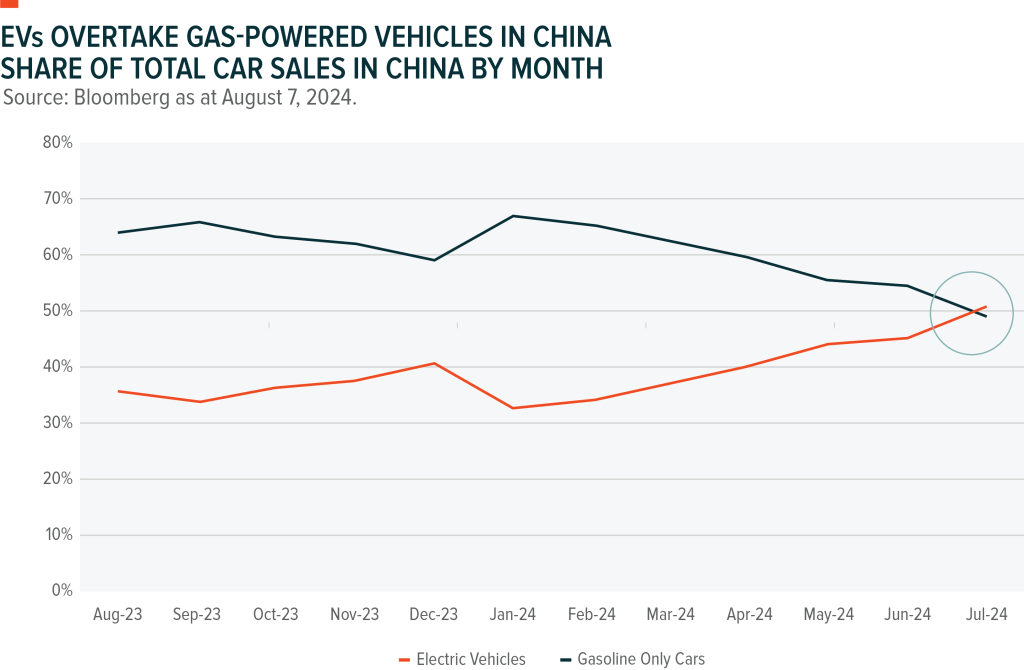

Lithium, a key component for electric vehicle (EV) batteries, has seen prices tumble dramatically after hitting record highs in 2021 and 2022. However, demand is expected to outpace supply, especially as EV adoption continues to accelerate, particularly in China, the world’s largest EV market, which sold over a million EVs in August 2024.

Uranium is also drawing renewed interest as nuclear energy emerges as a cleaner power source. Prices have surged in recent years, with projections suggesting global nuclear capacity could more than double by mid-century. This momentum signals a potentially strong outlook for uranium, highlighting growth opportunities in the broader industrial metals sector.

This blog gives an update on the key industrial metals shaping our future.

Copper

- Used in power cables, electric vehicles and solar farms.

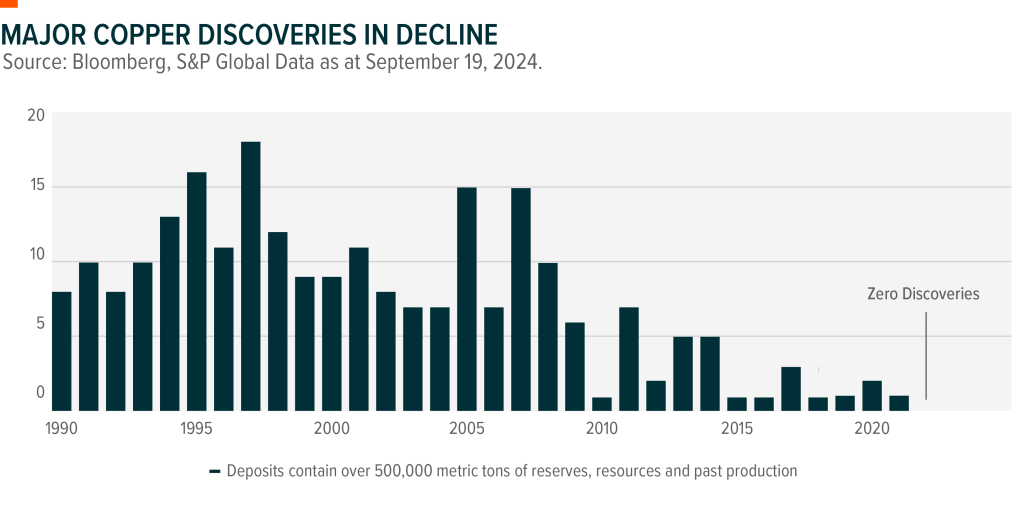

- The number of new major copper mines is declining.

- Goldman Sachs has cut its price forecast due to waning demand in China.

Copper is used in various industries and products necessary for countries to meet climate targets, including power cables, electric vehicles and solar farms. Many analysts are expecting a global copper shortfall in the medium to long term.

“Supply of copper is decreasing and at the same time demand is increasing,” says Brooke Thackray, Research Analyst at Global X. “Basic economics tells us that it is only a matter of time before there is upward pressure on the price of copper.”

Adding to the uneven supply picture is the fact that discoveries of new copper deposits are falling short:

Supply Projections

Mining giants are also warning that the growth of artificial intelligence (AI) will worsen a looming shortage of copper.

BHP Group Ltd., the world’s biggest miner by market capitalization, expects global copper demand to increase by 72% to 52.5 million tonnes per annum by 2050.

Data centres—home to the servers that run many of the world’s artificial intelligence (AI) services—are likely to worsen a copper shortfall as the adoption of AI applications continues. These applications will require more energy-intensive chips, adding to the energy needs of data centres. Copper is used in cabling to supply power, and cooling systems and to connect servers.

The copper market is in surplus this year due to poor demand on the back of recessionary fears, and that will continue next year as well, according to BHP forecasts, before reversing towards the end of this decade.

Bank of America analysts are projecting that copper prices will exceed US$10,000 per tonne by 2025, expecting prices to remain elevated with U.S. Federal Reserve (Fed) rate cuts. The price of copper remains strong due to high demand, constrained supply and increased investment in energy transition projects, analysts at the U.S. bank said.

Demand has increased due to global spending on energy infrastructure—especially grid expansion tied to decarbonization. Further supporting bullish sentiment on copper, while in China, grid investments have offset weaker demand from the housing sector. “Manufacturing activity should stabilize as the Fed cuts rates, so we maintain our constructive copper view into 2025,” the analysts said.

There was also a risk of disruption due to a labour dispute at Escondida, the world’s biggest copper mine, but a strike there that began on August 13, 2024, was resolved on August 16. From a supply-side mining perspective, the concentrate market continues to appear tight, and further disruptions have been registered and are in sight. In particular, due to decades of underinvestment, lengthy project delays, and mining disruptions, Codelco’s first-half production was 8.4% lower than its first half of the previous year.

Chinese Market Situation

China is a significant player in the world of copper: since 2000, the nation has accounted for 75% of all global smelter capacity growth. China serves as a major link in the process of turning raw copper into finished products.

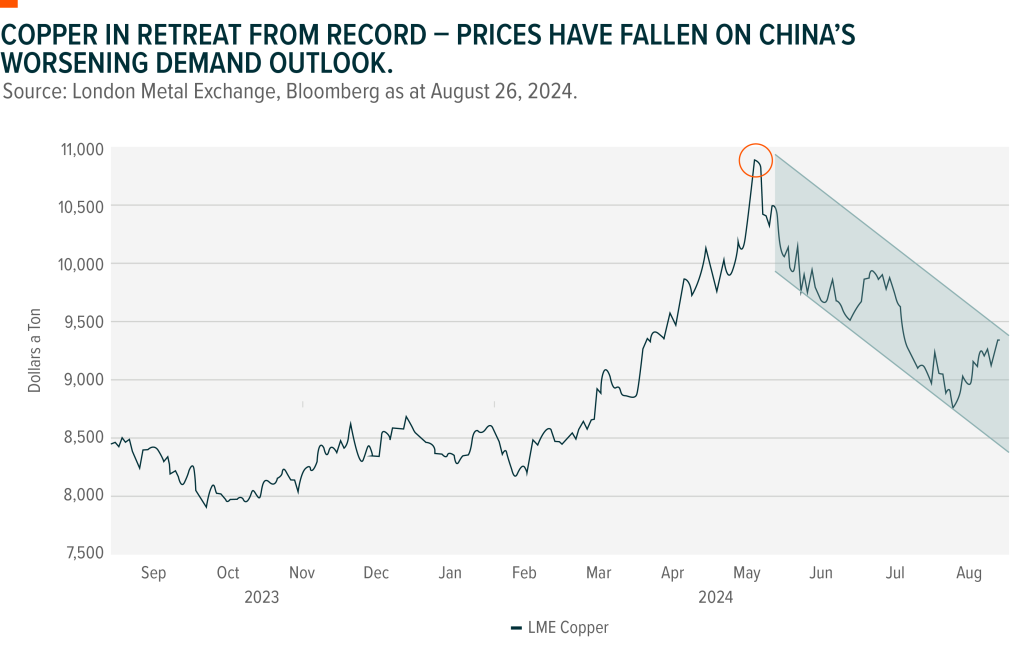

Goldman Sachs cut its price forecast for copper by citing shrinking demand in China.

“Softer-than-expected China commodity demand, as well as downside risks to China’s forward economic outlook, lead us to a more selective, less constructive tactical view of commodities,” the bank said in a Bloomberg News report.

Several factors, such as worsening global manufacturing data and disappointment following Chinese policy meetings, are driving risk-off sentiment. However, several announcements from Chinese entities highlight that copper demand could increase sooner rather than later.

In August China’s largest supplier of copper, Jiangxi Copper said it expects a global copper shortage to extend into the second half of 2024. Changes in Chinese tax law may reduce scrap processing and thus tighten supply, as scrap can be used as an alternate feedstock instead of ore concentrate, which has been scarce this year. Meanwhile, the State Grid Corp. of China, the world’s largest single consumer of copper – responsible for 80% of the country’s copper use – announced in July that it would increase spending by 13% to US$83 billion this year.

Lithium

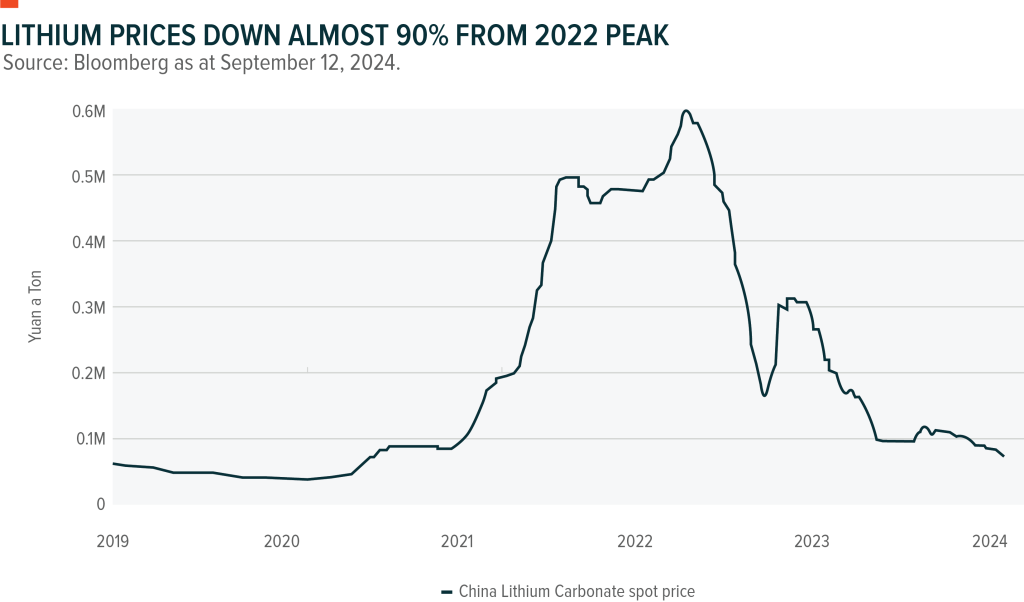

- Lithium-ion batteries are in high demand as the world shifts to a low-carbon economy, but lithium prices have dropped nearly 90% from their 2022 peak due to oversupply and slowing EV sales outside China.

- Countries such as the U.S., U.K., India, Germany, and Serbia are securing critical mineral supplies to reduce reliance on China and strengthen their EV supply chains.

- Lithium producers, like Albemarle, are adjusting strategies to cope with prolonged lower prices, cutting costs, and scaling back expansion plans.

With the world in the process of transitioning to a low-carbon economy, rechargeable lithium-ion batteries are in high demand – especially as countries such as Canada phase out the sale of new gasoline fuel vehicles over the coming years for battery-powered electric vehicles (EVs).

The key component in these rechargeable batteries is lithium: last year, approximately 88% of the world’s lithium supply came from brine resources in Argentina, Australia, Bolivia and Chile. Lithium prices have experienced significant volatility in recent years. After surging to record highs in 2021 and 2022, they’ve since plummeted, erasing all previous gains and now standing nearly 90% below their 2022 peak.

PRICE SLUMP; BUYING OPPORTUNITY?

While EV adoption, particularly in China, has driven strong demand, an accelerated increase in supply has outpaced this growth. Combined with slowing EV sales outside of China, this has contributed to the sharp decline in lithium prices.

Despite the current price slum the demand picture for lithium looks set to outstrip supply, as seen in this chart:

“Lithium has pulled back to levels not seen since early COVID,” says Global X’s Thackray. “Prices have now stabilized at levels which should allow for long-term appreciation as demand increases.”

A key driver of demand is China, the world’s largest EV market, which passed a significant milestone in July 2024 of having EV sales surpass 50% of total automobile sales for the first time.

Recent Developments

As a result of the current low and volatile price environment, numerous lithium producers have continued to hold down their expansion plans and work on decreasing costs.

Albemarle, a significant Australian producer of lithium, announced in July that it intends to initiate a “comprehensive review of its cost and operating structure” with the expectation that prices will remain “lower for longer.”

Still, there are recent developments that reinforce the positive long-term outlook on critical minerals.

Two Western nations have struck deals for critical minerals outside China. The U.S. started talks with Indonesia to help establish a sustainable supply chain for essential minerals. The U.K. also started similar mineral supply talks with Indonesia.

India has made a significant move by waiving import taxes on 25 commodities such as lithium, copper, cobalt and rare earth elements that are crucial for the electrification and clean energy industries, which may boost Indian processing and refining to ensure a steady supply of these minerals within that nation.

In Europe, Germany and Serbia have signed agreements for lithium excavation and EV battery manufacturing intending to cut the European Union’s dependency on Chinese lithium supply. With looming U.S. presidential elections and uncertainty over a possible change of political power, U.S. government departments are issuing grants and loans already approved under existing laws to bolster the domestic EV supply chain. In July, the U.S. Department of Energy announced $1.7 billion to support the conversion of 11 shuttered or at-risk auto manufacturing and assembly plants to produce and supply electric vehicles.

Uranium

- The Fukushima disaster depressed uranium markets, but Russia’s invasion of Ukraine triggered a price surge. Nuclear energy is gaining importance, with supply constraints already challenging the uranium market.

- Major uranium miner Kazatomprom increased production, while the IAEA projects nuclear capacity to rise 2.5 times by 2050, indicating nuclear energy’s growing role in clean energy.

- Investment sentiment is shifting, with some European firms investing in nuclear power. Uranium prices have spiked 233% since 2019, but supply remains insufficient to meet rising demand.

The 2011 Fukushima disaster resulted in governments pulling the plug on nuclear power, depressing the global uranium market. Russia’s 2022 invasion of Ukraine resulted in nations urgently seeking alternative sources of energy, contributing to a price surge in uranium.

Nuclear energy may be poised to play a pivotal role. The uranium market, essential for nuclear fuel, is already facing supply constraints, creating a challenge for suppliers and buyers alike.

“Consumers and investors are realizing that nuclear power is a “must” for a green energy future. There is no choice. The story only gets better from here,” Global X’s Thackray says.

MAJOR PLAYER FORWARD GUIDANCE

The world’s largest uranium miner, Kazatomprom, announced a rise in production in the first half of 2024, which led the Kazakhstan state-owned company to continue increasing output. Some 40% of global uranium production comes from Kazakhstan.

ENERGY DEMAND

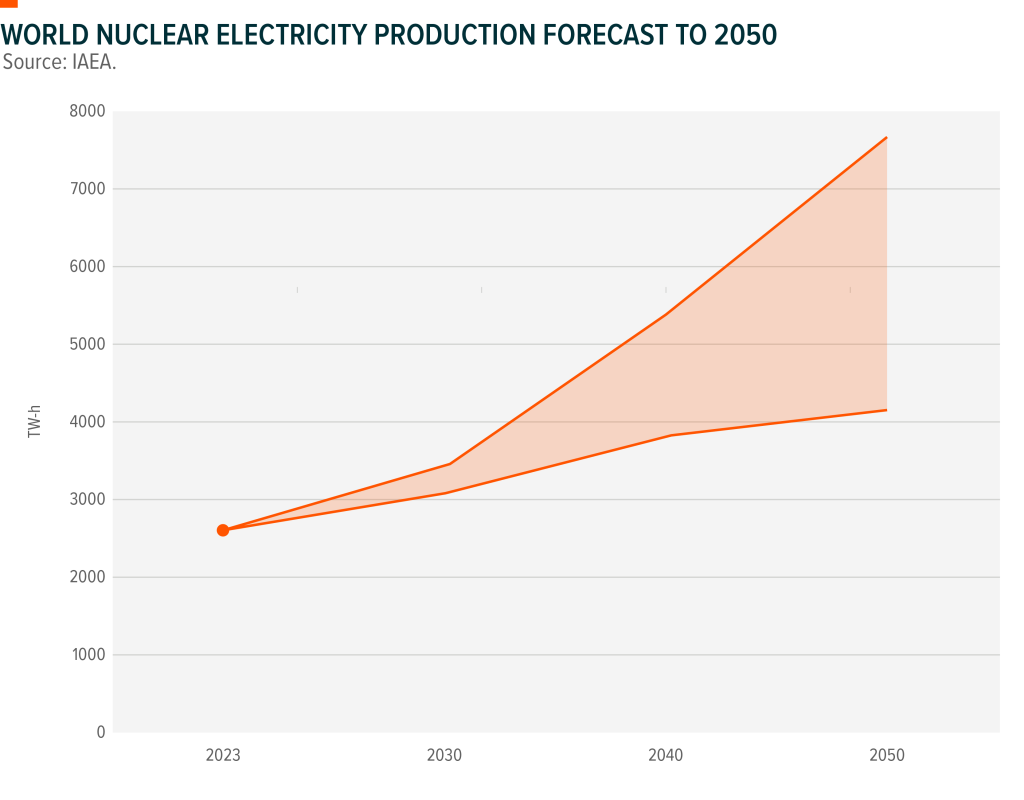

Projections from the United Nations’ International Atomic Energy Authority (IAEA) show that world nuclear capacity is now projected to increase by 2.5 times by 2050, according to the latest estimates from the IAEA. “The new IAEA projections reflect increasing acknowledgement of nuclear power as a clean and secure energy supply, as well as increasing interest in Small Modular Reactors to target both electric and non-electric applications to meet climate goals and foster sustainable development,” IAEA Director General Rafael Mariano Grossi said in a statement.

We have covered the role of data centres as a source of demand for copper. They are now a potential boon for the uranium industry: power-hungry data centres are also the reason behind Microsoft signing a deal to revive one of the mothballed reactors at Pennsylvania’s Three Mile Island. Over the 20 years of the deal, the reactor will provide 835 megawatts of electricity, enough to power 800,000 homes.

This a reminder that Microsoft not only runs the Azure cloud computing system, but it’s also a backer of the popular AI service ChatGPT.

Investment Sentiment

Major financial institutions are beginning to recognize the role that nuclear energy plays in the world’s energy transition process and that improving access to financing can help unlock the potential of nuclear power. Canada’s Brookfield, Bank of America, Barclays, Goldman Sachs and Morgan Stanley have pledged their support to provide experience, global presence, services and solutions to support the industry.

Investment industry sentiment appears to be shifting in Europe too. Firms such as Robeco, J O Hambro and Janus Henderson have emerged as global asset managers investing in nuclear power, a sector which was traditionally off-limits for environmentally-conscious investors.

Microsoft billionaire Bill Gates is prepared to invest billions of his own money into a nuclear energy startup that wants to build a commercial reactor in Wyoming.

The summer of 2024 saw mergers and acquisitions activity in the uranium sector heat up, with Paladin Energy agreeing to buy Canada’s Fission Uranium for $1.14 billion.

Global nuclear electricity generation rose 2% to 2602 terawatt hours (TWh) in 2023 from 2544 TWh in 2022, providing nine percent of the world’s electricity, according to the World Nuclear Association.

In 2023, the world’s nuclear reactors helped avoid 2.1 billion tonnes of carbon dioxide emissions from equivalent coal generation—that’s more than the annual emissions of almost every individual country, with only China, the US and India having higher national CO2 emissions.

The United Nations’ International Atomic Energy Agency said 413 nuclear reactors were operational at the end of 2023 with a global capacity of 371.5 gigawatts (GW). The atomic body estimates that nuclear-generating capacity is projected to reach 950 GW by 2050 – just over 2.5 times what it was last year.

While supply threats ease, uranium demand remains strong. Uranium’s long-term price is catching up to the spot level as nuclear energy opinion shifts.

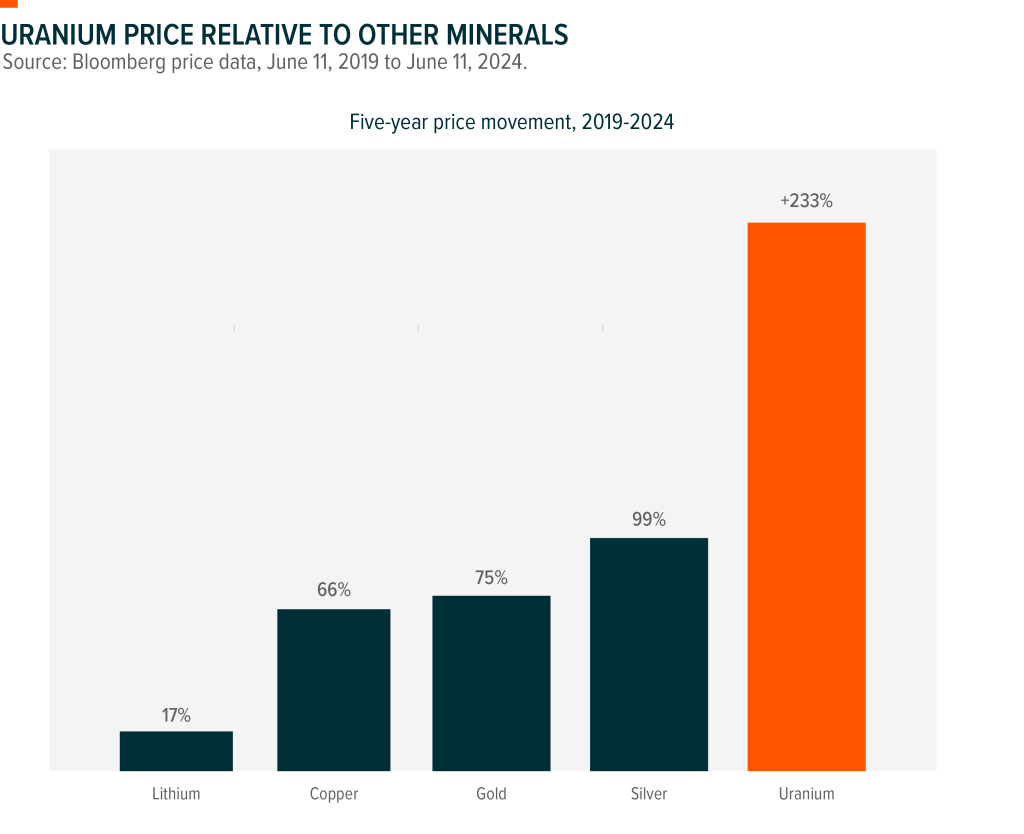

Price Spike

Since 2019, the price of the metallic element used as a nuclear fuel has risen by 233%.

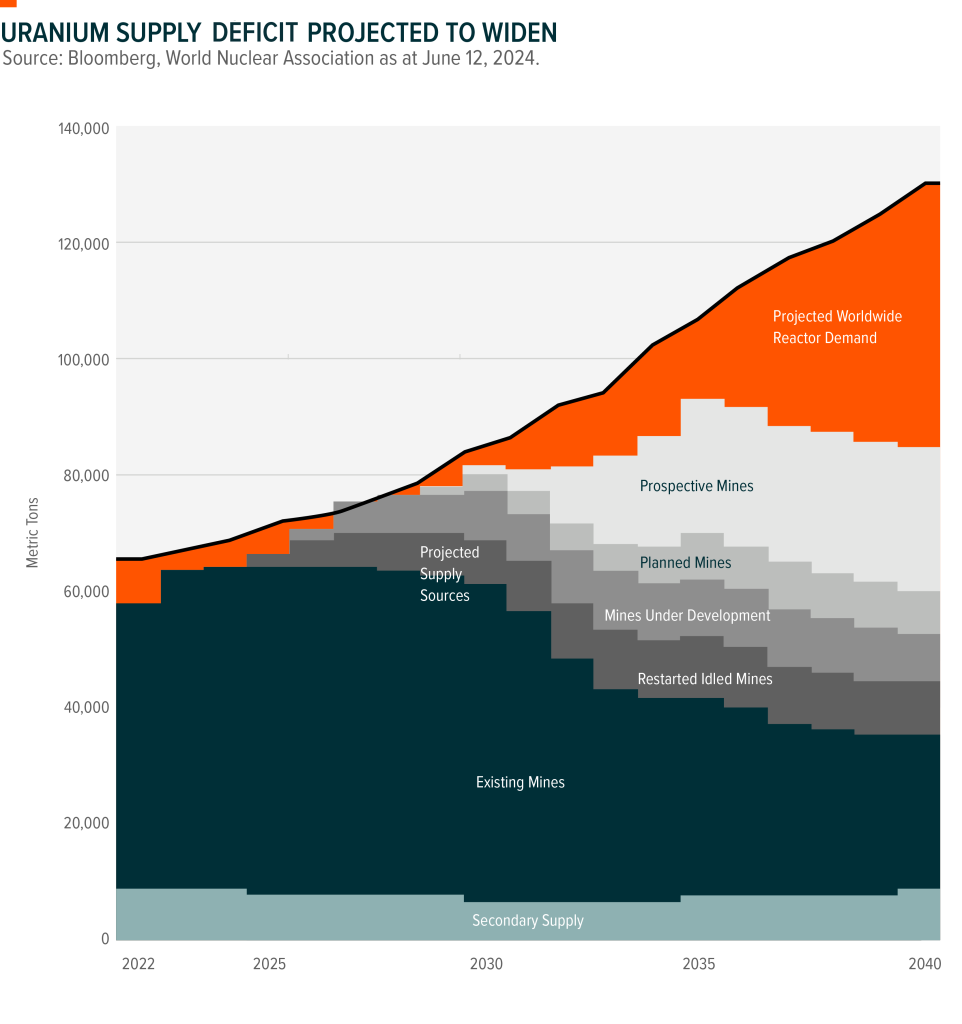

Supply Slump

On the supply side, there is currently not enough uranium to meet rising demand, as you can see from this chart:

RELATED ETFs

DISCLAIMERS

Commissions, management fees, and expenses all may be associated with an investment in products (the “Global X Funds”) managed by Global X Investments Canada Inc. The Global X Funds are not guaranteed, their values change frequently and past performance may not be repeated. Certain Global X Funds may have exposure to leveraged investment techniques that magnify gains and losses which may result in greater volatility in value and could be subject to aggressive investment risk and price volatility risk. Such risks are described in the prospectus. The prospectus contains important detailed information about the Global X Funds. Please read the relevant prospectus before investing.

Certain ETFs are alternative investment funds (“Alternative ETFs”) within the meaning of the National Instrument 81-102 Investment Funds (“NI 81-102”) and are permitted to use strategies generally prohibited by conventional mutual funds, such as the ability to invest more than 10% of their net asset value in securities of a single issuer, the ability to borrow cash, to short sell beyond the limits prescribed for conventional mutual funds and to employ leverage of up to 300% of net asset value. While these strategies will only be used in accordance with the investment objectives and strategies of the Alternative ETFs, during certain market conditions they may accelerate the risk that an investment in ETF Shares of such Alternative ETF decreases in value. The Alternative ETFs will comply with all requirements of NI 81-102, as such requirements may be modified by exemptive relief obtained on behalf of the ETF.

Certain statements may constitute a forward-looking statement, including those identified by the expression “expect” and similar expressions (including grammatical variations thereof). The forward-looking statements are not historical facts but reflect the author’s current expectations regarding future results or events. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. These and other factors should be considered carefully and readers should not place undue reliance on such forward-looking statements. These forward-looking statements are made as of the date hereof and the authors do not undertake to update any forward-looking statement that is contained herein, whether as a result of new information, future events or otherwise, unless required by applicable law.

This communication is intended for informational purposes only and does not constitute an offer to sell or the solicitation of an offer to purchase investment products (the “Global X Funds”) managed by Global X Investments Canada Inc. and is not, and should not be construed as, investment, tax, legal or accounting advice, and should not be relied upon in that regard. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. These investments may not be suitable to the circumstances of an investor.

All comments, opinions and views expressed are generally based on information available as of the date of publication and should not be considered as advice to purchase or to sell mentioned securities. Before making any investment decision, please consult your investment advisor or advisors.

For more information on Global X Investments Canada Inc. and its suite of ETFs, visit www.GlobalX.ca

Global X Investments Canada Inc. (“Global X”) is a wholly-owned subsidiary of Mirae Asset Global Investments Co., Ltd. (“Mirae Asset”), the Korea-based asset management entity of Mirae Asset Financial Group. Global X is a corporation existing under the laws of Canada and is the manager, investment manager and trustee of the Global X Funds.

© 2024 Global X Investments Canada Inc. All Rights Reserved.

Published October 9, 2024.

Categories: Articles, Insights

Topics: Commodities