Authored by Global X Research Team

The generative Artificial Intelligence (AI) boom extends far beyond chat assistants. The wider integration of large language models across various technology platforms and processes will need data centres and digital infrastructure capable of managing AI workloads effectively. As a result, new data centre construction is increasing and existing data centres are being retrofitted with graphics processing units (GPUs) and other AI hardware, leading to premium leasing rates. Because AI-optimized data centres consume more power, stakeholders are also starting to address power sourcing, potentially with alternative energies like renewables and nuclear. To deliver AI to the average consumer, investments in cell towers and AI devices are expected to grow as well.

We view these dynamics as catalysts that can accelerate growth and boost earnings for the broad data centre and digital infrastructure ecosystem. For investors, this means numerous opportunities to gain exposure to the AI paradigm shift.

Key Takeaways

- Industry stakeholders, led by hyperscalers, are rushing to invest in new data centres capable of delivering AI processing needs.

- New AI data centres and many existing data centres will be fitted with specialized AI hardware, creating opportunities for component suppliers and clean energy suppliers.

- Investments are likely to be ultimately directed towards enabling infrastructure such as cell towers and AI devices, which are needed for AI to achieve its potential at the consumer level.

AI Demand Spurs U.S. Data Centre Construction Activity

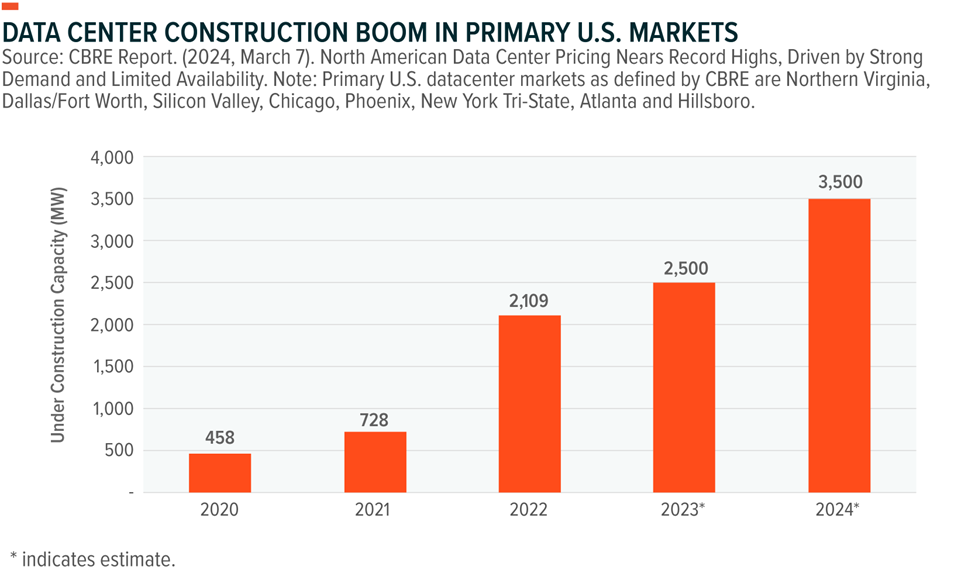

In the United States, primary data centre markets are expected to surpass 3,500 megawatts (MW) in construction activity in 2024, the highest level on record.1 In 2023, primary markets across the U.S. witnessed a nearly 25% year-over-year (YoY) increase in data centre supply, reaching 5,174 MW.2 In Europe, a record 273 MW of new capacity is expected to be built this year.3 The Dodge Momentum Index (DMI), a widely used measure of the value of non-residential building projects entering the planning phase, increased by 6.1% in April to 174.3, and another 2.7% in May to 179.0, largely driven by new data centre projects4. Over 25 construction projects valued at US$100 million or more in April, and an additional 19 projects in May, contributed to the DMI’s positive momentum5. Among the largest construction projects in the planning stages for April are several data centres, including the billion-dollar Convergent Tech Park in Remington, Virginia, and the US$630 million Dulles Digital Data Centre in Dulles, Virginia.6 For the month of May, the DMI benefitted from a US$495 million Prime Data Centre in Fort Worth, Texas and another US$481 million Prime Data Centre in Garland, Texas.7

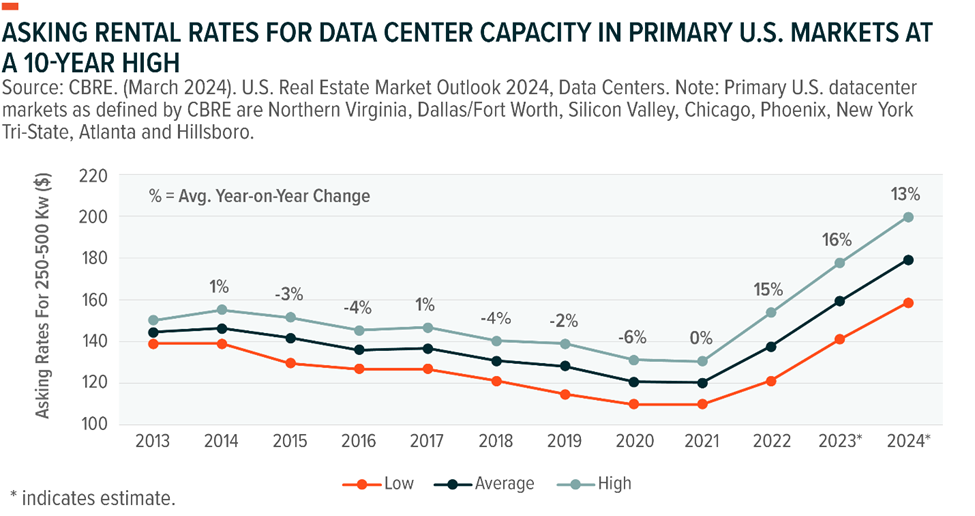

Meanwhile, vacancy rates for existing colocation-based data centres have reached record lows. According to CBRE, by the end of 2023, vacancy rates in primary U.S. markets fell to 3.7%.8 Simultaneously, rental rates for data centre capacity in primary U.S. markets are expected to increase by 13% year-on-year (YoY) in 2024, underscoring the growing demand amidst a capacity crunch.9

Additionally, investing aggressively in new capacity to power their own technology platforms and cloud computing businesses are the hyperscalers. As of 2023, the hyperscalers operated nearly 992 data centres worldwide, with capacity doubling over the past four years.10 The big four, Amazon, Meta Platforms, Microsoft, and Alphabet, are expected to spend US$200 billion on capital expenditures in 2024, an increase of more than 35% YoY.11

Amazon is planning a US$11 billion investment for a data centre complex in northern Indiana.12 Google is set to construct a US$2 billion data centre in Fort Wayne, Indiana, and spend an additional US$1 billion to improve existing facilities in Virginia.13 Google is also investing globally, with US$1.1 billion going to build a data centre in Finland and over US$5 billion for data centre expansion in Singapore.14 Meta is building a two-building data centre on a 328-acre campus in Davenport, Iowa, and it’s embarking on a multibillion-dollar data centre project in Cheyenne, Wyoming.15

According to an index calculated by New Statesman Media Group, Canada is the most energy-effective country in the world to build a data centre. Data centres use significant amounts of electricity to not only power servers and racks of hard drives, but also to keep them cool and operating efficiently.

With the prospect of climate change putting much of Silicon Valley at risk, could it only be a matter of time before technology companies begin to look towards cooler locales to house their data operations? The New Statesman’s data centre index shows Scandinavian and Baltic nations dominating its top ten, so there could be a case for housing heat-intensive data operations in cold climates, thereby improving their environmental credentials.

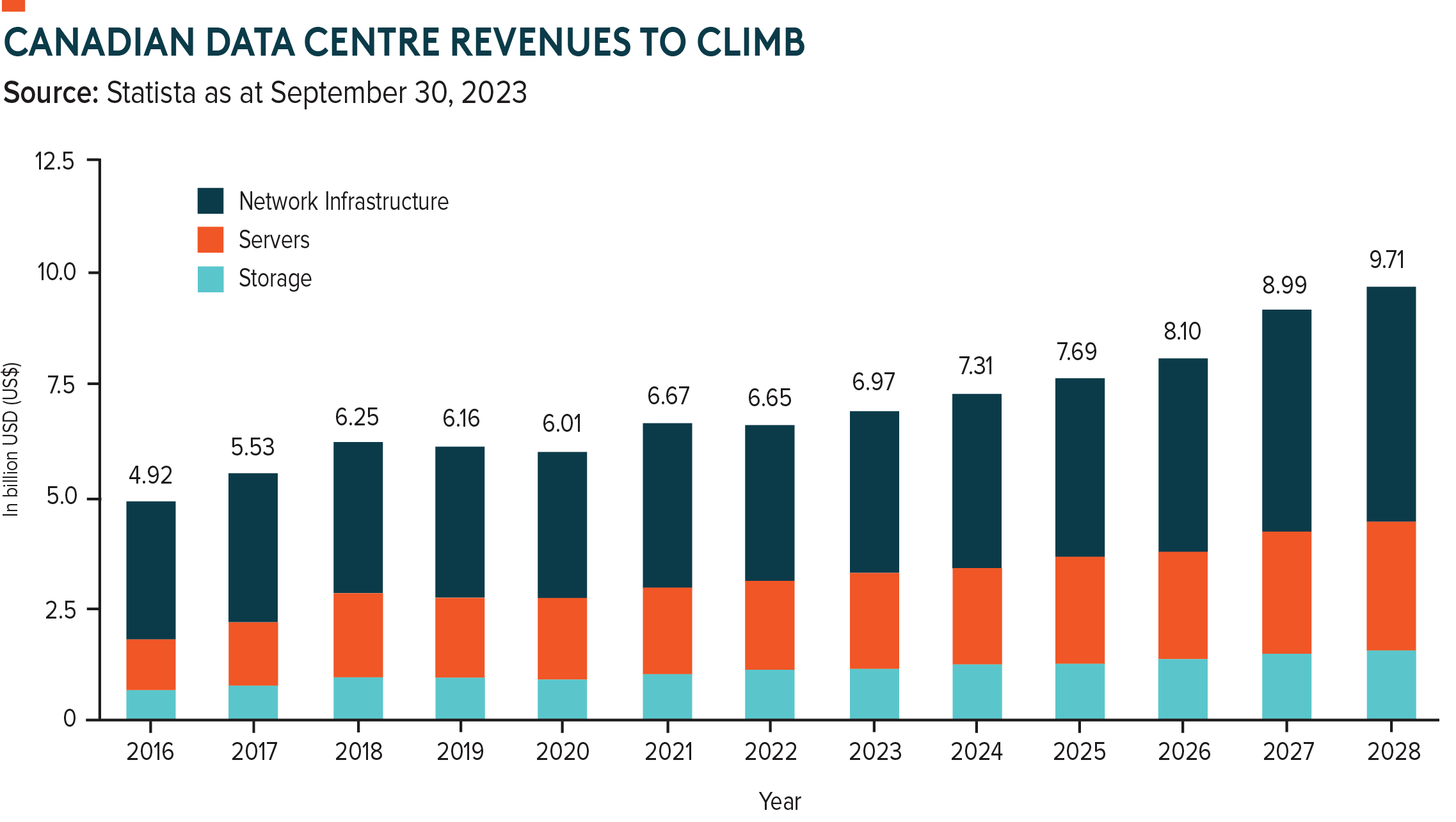

Due to Quebec’s cheap hydroelectric power (which is 36% cheaper than the U.S.) and cold winters, Microsoft is choosing La Belle Province to invest US$500 million in four data centres in the Quebec City area over the next two years. Fellow Magnificent Seven member Amazon opened its second Canadian AWS cloud computing region in Calgary, Alberta late last year. The western Canadian province is positioning itself as a place to invest in the data centre business. Data from Statista forecasts data centre revenue in Canada to reach US$9.71 billion by 2028.

AI Processing Creates Opportunities for New Hardware and New Energy

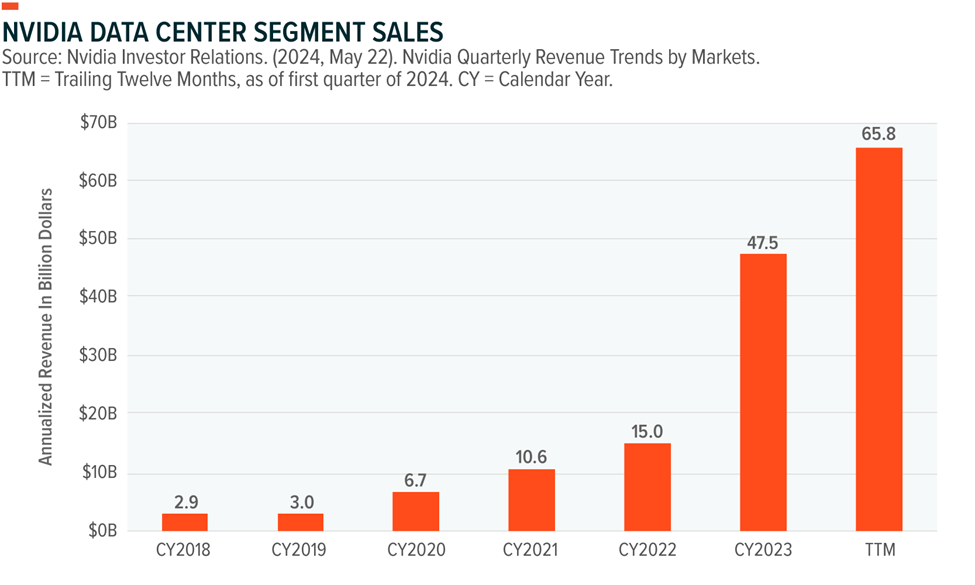

To process AI workloads, new data centres need a wide array of specialized hardware, which is creating unique tailwinds for specialized component providers. The most prominent example is Nvidia. In just the last 12 months, Nvidia sold nearly US$66 billion worth of GPUs to data centres, helping it ascend to the rarefied air of a US$3.3 trillion market cap.16 We expect spending on data centre accelerators alone to grow at a nearly 30% annual growth rate to top US$165 billion by 2030.17

Broadcom, one of the largest suppliers of AI networking solutions and application specific integrated chips (ASICs) for AI processing to companies like Meta Platforms and Alphabet, projects its AI segment revenues to grow by over 50% YoY to US$11 billion in Fiscal Year 2024.18 Also, chipmakers Intel and AMD launched new products, including data centre CPU chips, which are expected to be used widely for AI inferencing applications.19 Other prime examples of the infrastructure needed to support AI workloads include specialized cooling systems for data centres. High-capacity memory and fast storage solutions are also essential to handle the vast amounts of data processed by AI applications, such as those supplied by SK Hynix or Micron.20

Another significant consideration with AI hardware growth is that it comes with severe power trade-offs. An average ChatGPT query consumes 10 times more power than a regular Google search, resulting in an AI-first data centre requiring nearly 2.5 times more electricity on average than a traditional data centre.21 In primary U.S. data centre markets, where new data centre construction activity increased by 25% in the first half of 2023, power supply demands increased 19.2% YoY.22

Data centres currently account for 1-1.5% of global electricity use, but by the end of this decade, it’s expected to exceed 5%.23 Because conventional grids are unable to supply this increase, data centre companies must resolve their power supply, which is a hurdle that can extend construction completion timelines by 24-72 months.24 Potential solutions include the use of nuclear and renewable energies. For example, Amazon recently acquired a US$650 million data centre project from Talen Energy close to a nuclear power station in Pennsylvania.25 Microsoft and Google joined hands for a partnership with Nucor to source geothermal, clean hydrogen, and other clean energy sources.26

Infrastructure Density and Enhanced Devices Crucial to Bringing AI to Users

Existing mobile connectivity infrastructure is insufficient to handle the massive amounts of data AI systems generate. Seamless connectivity and data transmission to end users require an extensive expansion and enhancement of cell towers, particularly in dense urban areas. A likely growth segment is small cell towers, which can increase service densification. U.S. cell tower leader Crown Castle expects demand for small cell towers to grow significantly in 2024, even as the telecom industry braces for a 10% drop in capital expenditure.27 Crown Castle’s small cell tower business grew 6% YoY in 2023.28

Edge data centres, along with content delivery networks (CDNs), are another segment that can play a crucial role in reducing latency and enabling AI systems to process data closer to end users and applications. Edge computing facilitates real-time processing and response which is vital for consumer applications and real-time connectivity.

Also, devices are likely to be optimized for AI. Local inference processing, where AI computations are done directly on the device, will become increasingly important. Smartphone giants like Apple are already moving in that direction. Apple’s latest announcements include the launch of Apple Intelligence, a device-based AI assistant capable of working only on Apple’s latest M-chip hardware and iOS 18.29 This development signals the likelihood of a smartphone upgrade cycle, which could catalyze growth for a long list of component vendors and device manufacturers. Laptops, wearables, internet of things systems, and industrial automation setups will require upgrades, including specialized low-power chips and components to efficiently handle AI tasks.

Conclusion: Data Centre & Digital Infrastructure Value Chain Appear Well-Positioned

We believe that the digital infrastructure value chain presents highly investable opportunities as corporate investments in AI continue to grow. Data centre companies can leverage newly built and enhanced AI processing capacity to upcharge and boost their sales and earnings. Chip and component manufacturers can benefit from an upgrade cycle in processing hardware and devices, fueled by growing construction of new data centres. Cell tower companies, edge computing platforms, and device makers will provide critical infrastructure. In our view, exposure to these pillars of the AI ecosystem offers an attractive way to play AI’s proliferation.

Related ETFs

Global X Semiconductor Index ETF (CHPS, CHPS.U)

Sources:

- CBRE Report. (March 7, 2024). North American Data Centre Pricing Nears Record Highs, Driven by Strong Demand and Limited Availability.

- CBRE Report. (March 6, 2024). North America Data Centre Trends H2 2023.

- CBRE Report. (March 7, 2024). North American Data Centre Pricing Nears Record Highs, Driven by Strong Demand and Limited Availability.

- Dodge Construction Network. (June 7, 2024). Dodge Momentum Index Improved 3% in May.

- Dodge Construction Network. (June 7, 2024). Dodge Momentum Index Improved 3% in May.

- Data Centre Knowledge. (June 5, 2024). New Data Centre Developments: June 2024.

- Dodge Construction Network. (June 7, 2024). Dodge Momentum Index Improved 3% in May.

- Sunbird. (June 21, 2024). Colo Vacancy Rates Near Record Low: What Can You Do?.

- CBRE. (March 2024). U.S. Real Estate Market Outlook 2024, Data Centres.

- Synergy Research. (April 17, 2024). Hyperscale Data Centres Hit the Thousand Mark; Total Capacity is Doubling Every Four Years.

- Forbes. (May 9, 2024). Big Tech Q1 Earnings: AI Capex Increases As AI-Related Gains Continue.

- Reuters. (April 25, 2024). Amazon to invest US$11 billion in Indiana to build data centres.

- Reuters. (April 26, 2024). Google plans US$3 billion data centre investment in Indiana, Virginia.

- Forbes. (June 3, 2024). Google’s Singapore Investments Jump Five-Fold to US$5 Billion.

- Data Centre Dynamics. (May 21, 2024). Meta named as company behind 328-acre data centre in Davenport, Iowa.

- Nvidia Investor Relations. (May 22, 2024). NVIDIA QUARTERLY REVENUE TREND BY MARKETS

- Global X estimates, computed as of December 2023, with information from Precedence Research, 2023; Bloomberg, 2023; Statista, 2022.

- Reuters. (June 12, 2024). Broadcom boosts revenue forecast from AI chips, unveils stock split.

- CNBC. (June 3, 2024). AMD announces new AI chips amid intensifying competition with Nvidia, Intel.

- Forbes. (June 10, 2024). AI is Driving Memory and Storage Demand and Production Introductions.

- Goldman Sachs. (May 14, 2024). AI is poised to drive 160% increase in data centre power demand.

- CBRE. (2024). Data Centres, U.S. Real Estate Market Outlook 2024.

- Ibid.

- Goldman Sachs. (May 14, 2024). AI is poised to drive 160% increase in data centre power demand.

- Data Centre Dynamics. (March 4, 2024). AWS acquires Talen’s nuclear data centre campus in Pennsylvania.

- Google, The Keyword. (March 19, 2024). A new initiative with Microsoft and Nucor to accelerate advanced clean electricity technologies.

- RCR Wireless. (January 2024). Despite carrier capex contraction, Crown Castle sees ‘significant’ small cell demand.

- Ibid.

- Vox. (June 11, 2024). Apple’s convincing case that AI doesn’t have to be scary.

DISCLAIMERS

Commissions, management fees and expenses all may be associated with an investment in products (the “Global X Funds”) managed by Global X Investments Canada Inc. The Global X Funds are not guaranteed, their values change frequently and past performance may not be repeated. The prospectus contains important detailed information about the Global X Funds. Please read the relevant prospectus before investing.

Certain statements may constitute a forward-looking statement, including those identified by the expression “expect” and similar expressions (including grammatical variations thereof). The forward-looking statements are not historical facts but reflect the author’s current expectations regarding future results or events. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. These and other factors should be considered carefully and readers should not place undue reliance on such forward-looking statements. These forward-looking statements are made as of the date hereof and the authors do not undertake to update any forward-looking statement that is contained herein, whether as a result of new information, future events or otherwise, unless required by applicable law.

This communication is intended for informational purposes only and does not constitute an offer to sell or the solicitation of an offer to purchase investment products (the “Global X Funds”) managed by Global X Investments Canada Inc. and is not, and should not be construed as, investment, tax, legal or accounting advice, and should not be relied upon in that regard. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. These investments may not be suitable to the circumstances of an investor.

All comments, opinions and views expressed are generally based on information available as of the date of publication and should not be considered as advice to purchase or to sell mentioned securities. Before making any investment decision, please consult your investment advisor or advisors.

Global X Investments Canada Inc. (“Global X”) is a wholly owned subsidiary of Mirae Asset Global Investments Co., Ltd. (“Mirae Asset”), the Korea-based asset management entity of Mirae Asset Financial Group. Global X is a corporation existing under the laws of Canada and is the manager, investment manager and trustee of the Global X Funds.

Published July 22, 2024

Categories: Articles, Insights

Topics: Semiconductors, Technology